Earnings Analysis: Uber Q1 2023

Summary: Uber continues to impress investors with strong bookings growth and disciplined expense management. For us, we’re most impressed with Uber’s ability to launch new products and features while keeping costs in check, a testament to the company’s management team.

We believe Uber remains an attractive long-term investment as the company ranks highly in all of our investment criteria:

Management team

Product value proposition

Product improvement strategy

Capital allocation strategy

Lastly, Uber’s price point remains attractive relative to the overall market right now. Although the stock jumped more then 10% after this quarter’s strong earnings report, it is still within our investment price range.

Previous target price: $28.01

New target price: $28.79

Current share price: $37.84

Bookings

Uber continues to find ways to grow. Bookings, which represent the total dollar amount of an Uber ride or Uber Eats delivery, have remained strong and steady in the company’s recovery from the pandemic.

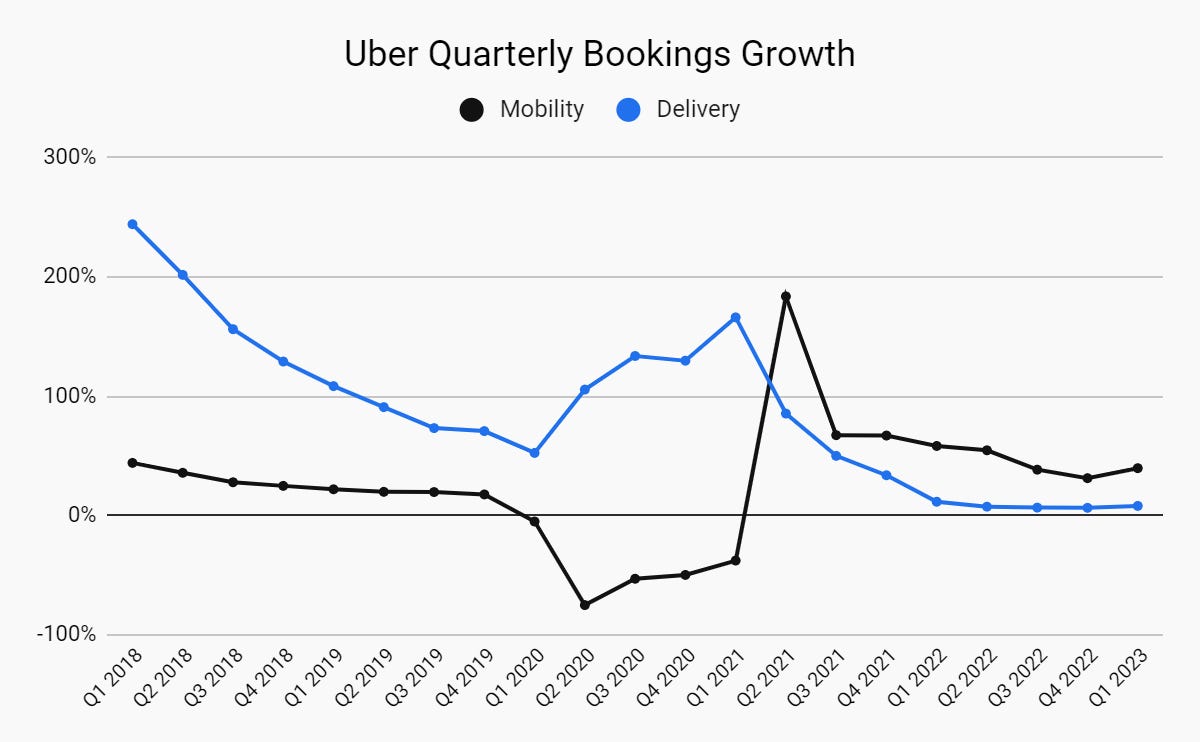

Bookings grew 19% this quarter compared to Q1 2022 which marks nine straight quarters of bookings growth.

Uber’s bookings growth has been a tale of two segments.

Uber’s mobility segment (mainly ridesharing in the US) dropped off a cliff as the pandemic hit in 2020. Since then, the business has grown at an impressive rate, including 40% growth last quarter.

The delivery segment (Uber Eats) had an opposite story. Food delivery revenues spiked as people stayed home from restaurants in 2020 and have since stabilized at a mid-single digit growth rate.

Many investors did not foresee Uber maintaining such solid growth which is why Uber’s stock is up 64% in the past year. So what is driving this growth?

Growth Strategy

Behind Uber’s growth is an impressive membership and platform strategy.

Uber’s membership strategy is to increase its customer base by rolling out new products around the world. Grocery delivery and taxi-hailing are two products Uber is betting on to reach more customers around the world.

The strategy seems to be paying off as Uber has reported strong growth in these areas as well as double digit monthly active customer growth in each of the last eight quarters.

Additionally, Uber is realizing the benefits of its Uber One membership that launched18 months ago. The membership program starts at $10 per month and gives members 5% off Uber rides and $0 delivery fees on Uber Eats. Why did Uber create this program?

Here is Uber CEO Dara Khosrowshahi describing the strategy behind it:

“The goal of Uber One is really we are giving a discount to our best customers in order to drive frequency, and we continue to see Uber One members spend four times more than nonmembers. Retention is 15% higher than nonmembers as well. And Uber One continues to be a higher and higher percentage of our bookings. It's about 27% now, and we have a target of driving that to 50-plus percent.”

The strategy is working. He mentions that 27% of bookings are from Uber One members and is likely a factor behind Uber’s quarterly trips (number of rideshare rides and Uber Eats deliveries) hitting record highs:

The second strategy is the “platform”. What this means is that once Uber gets a customer to download their app, either for ridesharing or food delivery, they are able to convert that customer to use their other product since they already have the app.

The strategy makes sense. If someone comes to Uber for ridesharing, it should be pretty easy to also get them to use Uber Eats.

Here is Khosrowshahi again discussing this strategy:

“We're benefiting from the power of the platform, very cheap audience from our rides business. Remember, we get more new leaders from our rides app than we do from Google and Facebook and Instagram combined at about a quarter of the cost. So that is a very significant structural advantage that is assisting our delivery business.”

That fact is pretty incredible. Most businesses, especially growing consumer businesses, spend tremendous resources on marketing strategies and advertising costs. Uber is using the age old cross-sell technique to its two consumer businesses in a way which its competitors that don’t offer multiple products can’t.

For evidence that this is working, let’s take a look at Uber’s sales and marketing expense over the past four years:

Sales and marketing expense, which includes advertising costs and salaries for salespeople and the marketing team, has remained relatively steady compared to how fast revenue has grown. The blue columns show that Uber spends roughly $1.25 billion per quarter on sales and marketing.

The black line shows sales and marketing expense as a percent of Uber’s revenue for that quarter. This ratio is a good proxy for operating leverage - the ability for a company to grow revenue while keeping costs low.

In Q1 2019, sales and marketing expense made up 34% of Uber’s revenue. This quarter, that number is only 14%.

On the financial side, Uber hopes to reach operating profitability in at least one quarter this fiscal year. That means being profitable from its main business before accounting for taxes and interest expense.

The company is on its way to achieving that as revenue continues to grow faster than expenses as seen in the chart below.

Valuation

It is hard not to admire the results of Uber’s business this past year. After recording unfathomable losses for most of its life, Uber is now a few quarters away from being profitable.

We believe Uber’s management team, network effects, and platform strategy make Uber an attractive long-term investment. Even at this price point, the stock is at a relatively attractive price compared to the overall market.

In a time when most companies are scaling back investments, Uber is strategically pushing new products and investments to expand its market share across its core businesses. The results will speak for themselves as we await the company’s first ever profitable quarter.

Investment research disclaimer: the financial valuation methods, target prices, and model assumptions discussed above are for educational and informational purposes only and reflect only our views at the time of publishing. The information and/or strategies above should not be used to make investment decisions. Past results are not predictive of future performance and future investment proceeds are not risk free and cannot be guaranteed. We are not a registered investment advisor or broker and all investment decisions must be made independently of the educational research published here.