Summary: Spotify crushed subscriber growth expectations, as it has done for several quarters in a row now. However, the company has made minimal progress on average revenue per user (ARPU) growth or expense management, which leaves us with doubts about how profitable Spotify can be in the long-run.

Spotify’s executive team called 2022 an “investment year” (a nice spin on the fact they hired too many people and laid off 600 employees in January). They also said Spotify will increase efficiency this year (just like everybody else). Expense management is mission critical to Spotify’s long-term success due to the music streaming business model, which has relatively low margins as record labels demand a large cut of streaming revenues.

Despite our doubts, we have upgraded our price target on Spotify’s stock as strong subscriber growth and management’s focus on profitability through expense management and prices increases is step in the right direction.

Previous target price: $26.22

New target price: $32.77

Current stock price: $137.39

Let’s go through the numbers.

Quick reminder: Spotify is a European company and reports their financial statements in Euros - so all financial metrics referenced here will be in Euros, despite the $ symbol.

Subscribers

The number everyone will be talking about from Spotify’s earnings release will be 5 million, the number of new subscribers Spotify added in Q1, compared to the company’s projection of 2 million added users.

While this represents an impressive 15% YoY increase in subscribers from Q1 2022, there is likely some gamesmanship going on here.

In short, Spotify is relying on growing its premium subscriber base to keep investors happy to make up for the company blowing through $500 million in cash last year. Spotify’s game plan is likely to under-promise on subscribers guidance such that they can over-deliver on subscribers each earnings report.

This tactic is one of the oldest tricks in the book but is important to call out to paint a more holistic picture of a company’s strategy.

As the company adds paid subscribers, they have done even better with adding free users. Spotify continues to add free users at a 20% YoY rate over the past five quarters.

Our view is that Spotify’s product continues to be the best in class, which has helped the company grow with a pretty limited marketing budget. The company is also growing the most in emerging markets where users are less likely to upgrade to a premium plan.

Let’s now turn our attention to how Spotify is monetizing these users.

Average Revenue Per User (ARPU)

Spotify makes about $4.40 per premium subscriber each month and about 46 cents per non-paying user each month. This probably sounds low considering a Spotify subscription is $10 per month, but remember that plans are priced differently in each country and that users in a family plan have a significantly lower revenue per user.

As Spotify grows, they are also adding more subscribers in countries with lower priced premium plans. This trend is a similar to what Disney and Netflix have faced as they expand internationally.

Additionally, while Spotify doesn’t disclose how many users are part of family plans, we know they must play a part in the company’s APRU declining from 2019 to now.

Revenue

Now that we have looked at both subscriber and ARPU growth, we know Spotify’s revenue is supported by increasing subscriber growth and not price increases.

Spotify is planning to raise prices in more markets as its prices are now below its largest competitors. As we mentioned before however, Spotify is likely hesitant to raising prices at the moment in order to maintain their strong subscriber growth.

So if subscriber and revenue growth is so strong, why is our price target so below the market’s?

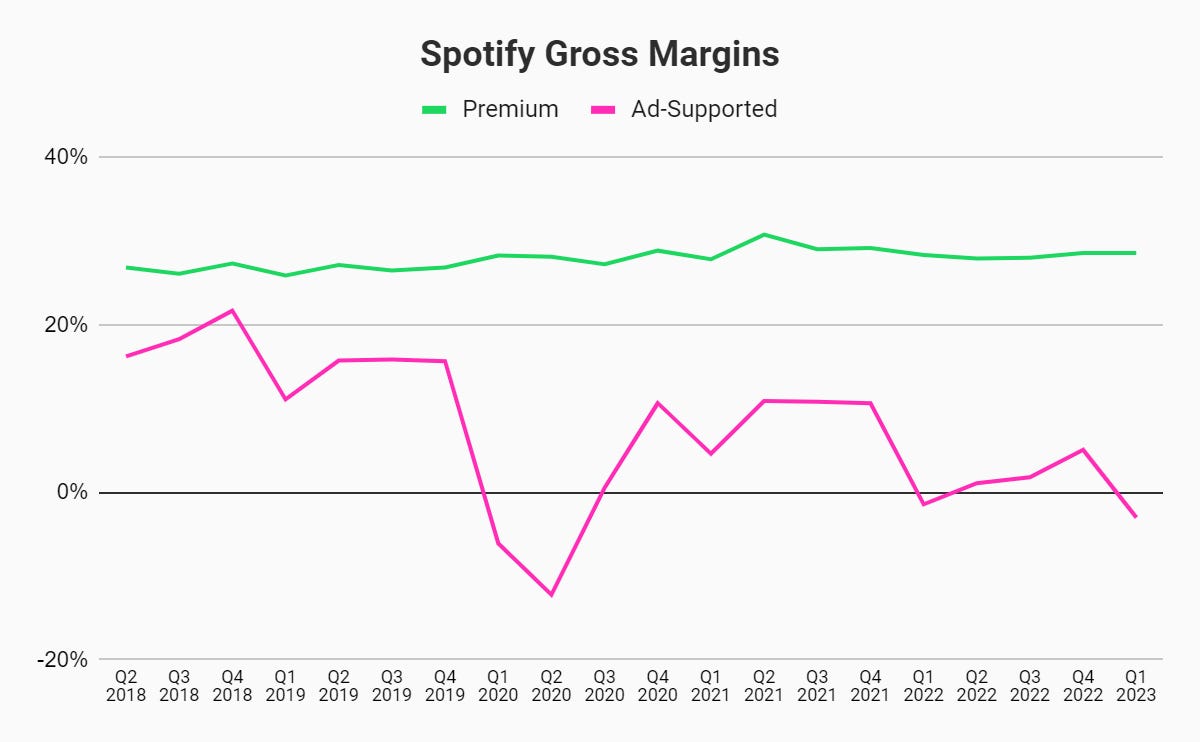

Gross Margins

Spotify’s gross margins have always hovered around 25% as the company is tied to deals with record labels that force Spotify to pay a portion of their revenue to the record labels as royalties.

These royalty payments make up the vast majority of Spotify’s cost of revenue as the company previously disclosed that 70% of all revenue is given back to artists and labels. This means their margins are only 30%, with an additional 5% accounting for costs to operate the service like cloud computing and credit card fees.

You likely noticed in the chart above that gross margins for the ad-supported business have fallen since 2019 and are actually negative at the moment. That means for every dollar that Spotify makes in revenue from an ad-supported user, it actually costs them more than one dollar to provide that content on average.

This is partially attributable to Spotify’s spending on podcasts over the past three years as they sign exclusive deals with big name talent. The company has stated they are losing money overall on podcasts but are aiming for podcasts to one day have 30%+ margins, similar to their music streaming business.

Operating Costs

Due to music streaming’s low margin business model, a sharp focus on operating expenses is crucial. When you are only left with 30% of your revenue after royalties, it means every dollar in operating expenses must be spent carefully.

For reference to Spotify’s 25% gross margin, Netflix’s still maintains a 40% gross margin despite spending $17 billion per year on tv and movie content. So essentially, Spotify has significantly less margin to work with than Netflix, who is known for being the largest spender in the TV streaming industry.

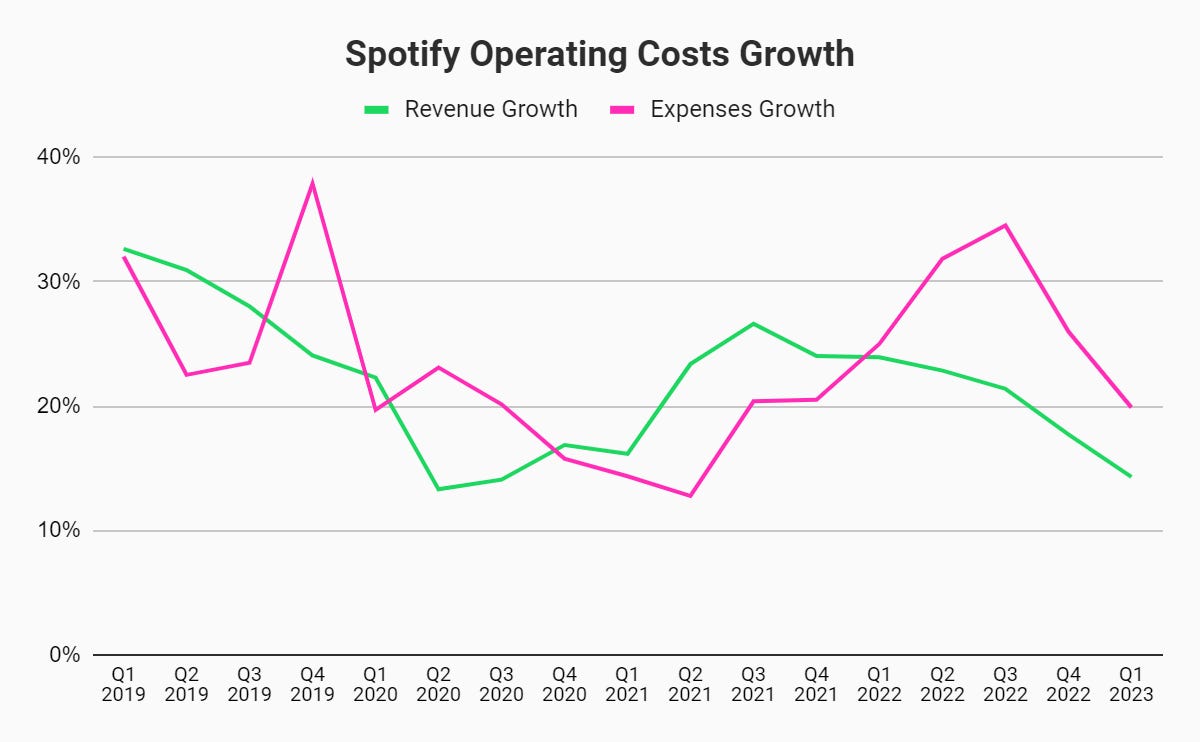

To make matters worse, Spotify did not handle expenses well last year.

The pink line in the chart above shows how fast operating expenses grew compared to revenue. In periods where the pink line is above the green line, that means Spotify lost operating leverage.

Operating leverage is critical for platform and marketplace businesses. A platform company should be scaling, mean it should be spending less dollars for every additional dollar of revenue. That is not the case with Spotify and is our biggest concern with the business model.

Spotify’s operating expenses as a percent of revenues have actually increased since 2019, the exact opposite of what you would expect from a great platform company.

Airbnb is an example of how a platform and marketplace company should operate. Airbnb has decreased their operating expenses as a percent of revenue by 30% from 2019 to 2022 which has allowed them to become incredibly profitable.

Airbnb’s management team has had a very direct focus on reducing operating expenses ever since the pandemic almost bankrupted them. Spotify on the other hand fell into the same trap that almost every other company fell into. They hired too many people and ignored expense management in order to keep up with demand.

This left the company in a difficult position in January when they laid off 6% of their workforce, around 600 employees. When asked about further layoffs in the earnings call today, the company’s management did not rule out additional cuts to headcount.

Free Cash Flow

The result of Spotify’s year of “investment” has cost the company $786 million in cash outflows in the last 12 months.

The negative cash flow will not kill the company as they are sitting on $4.5 billion in cash/investments with only $1.5 billion of debt - but it has been a wake up call to investors that Spotify’s low margin business needs to run more efficiently.

While companies like Google and Facebook can get away with over-hiring and still produce $10 billion free cash flow quarters, Spotify is not such a company.

We project that Spotify will not become free cash flow positive until 2025. To reach breakeven, the company will need to get operating expenses down from 30% of revenues to 23-24% of revenues. Without more layoffs or serious cost cutting, they will only be able to hit this target through growth, which will take time.

Valuation

We value every company using a discounted cash flow analysis. Using our consistent 10% discount rate, we put Spotify’s enterprise value at $2.9 billion with net cash at $3.4 billion, giving us an equity value of $6.3 billion. If we divide this by the number of shares outstanding, 194 million, we are left with our price target of $32.77 per share. This target price is currently 76% below Spotify’s closing price today at $138.20.

While Spotify has created a product that consumers love, the economics of the music streaming business makes it difficult for any standalone streaming company to produce strong free cash flows, even at a scale like Spotify’s. We like Spotify’s move into podcasts but it has come at a steep cost which has so far outweighed its monetary value created.

For Spotify to reach its current valuation of $27 billion, we estimate the company would need to double revenue over the next seven years and hit 10% operating margins in the same time frame. At present, we believe that is unachievable, hence our current target price.

While Spotify has hit two of our investment criteria: a strong product value proposition and product improvement execution, the company’s subpar capital allocation strategy and management decisions do not make up the difference between our target price and the current stock price for Spotify to be a worthwhile investment for us at the moment.

Investment research disclaimer: the financial valuation methods, target prices, and model assumptions discussed above are for educational and informational purposes only and reflect only our views at the time of publishing. The information and/or strategies above should not be used to make investment decisions. Past results are not predictive of future performance and future investment proceeds are not risk free and cannot be guaranteed. We are not a registered investment advisor or broker and all investment decisions must be made independently of the educational research published here.