Earnings Analysis: Peloton Q4 2023

Summary: Peloton is trading at all-time lows as the company struggles to grow revenue despite numerous new initiatives to expand the business.

We have downgraded Peloton’s revenue forecast to reflect the company’s struggle to grow revenue.

Previous price target: $12.05

New price target: $5.01

Current share price: $5.07

Peloton’s Revenue Problem

“Not since I stepped into the CEO role have we had as many new irons in the fire to drive both short- and long-term growth. It’s a big deal, and it serves to remind us that Peloton's transformation continues with urgency to pursue sustained, profitable growth. I expect these initiatives to accelerate our growth this fiscal year, but not this quarter. For the most part we have no operating history with these new initiatives which means we don’t know how to model their impact on our growth. For financial planning purposes this means we’ve forecast some of the expense and none of the revenue these initiatives might generate in FY24. That means there could be significant upside to our financial performance later this year, or none at all. I’m signaling significant potential upside but considerable uncertainty, in the spirit of radical transparency.” - Peloton CEO Barry McCarthy in August.

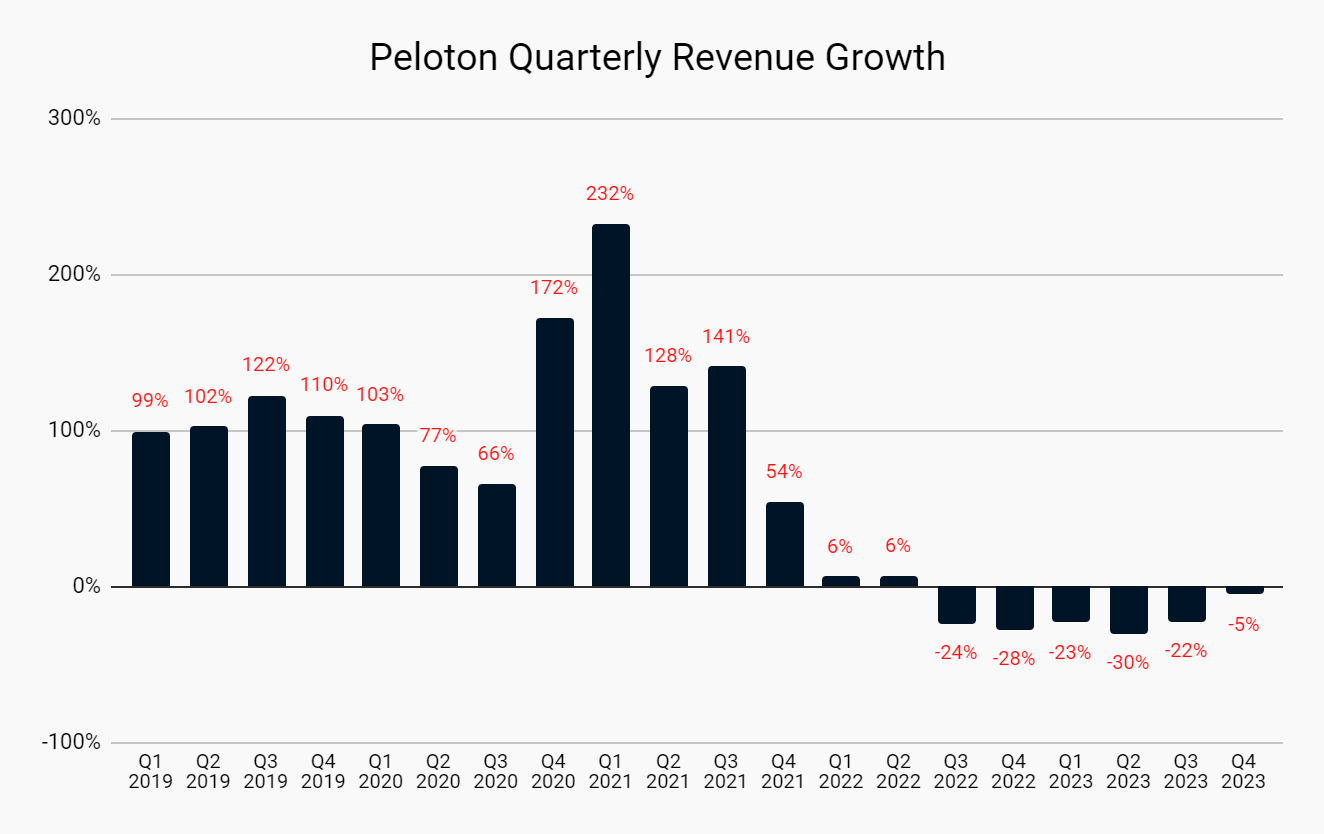

Peloton just reported their sixth straight quarter of revenue declines even as they have dedicated significant resources on new revenue initiatives.

Let’s take a look at the some of the ways Peloton is trying to jumpstart revenue growth:

Partnered with Amazon and Dick’s Sporting Goods to sell bikes and equipment through their stores and websites instead of exclusively selling through themselves since founding.

Launched Fitness-as-a-Service, a program where customers can rent their Peloton equipment instead of purchasing upfront.

Started selling refurbished equipment from customers who returned their bikes.

Partnered with Liverpool Football Club and the University of Michigan as their official fitness equipment sponsor.

Formed a strategic partnership with Lululemon to cross-sell Peloton subscriptions to Lululemon loyalty members.

Restructured their commercial business to improve sales to commercial clients.

Partnered with Hilton Hotels to place a Peloton bike in every Hilton hotel gym in the United States.

The results so far? Not material.

Peloton’s equipment sales (stationary bikes and treadmills) have plummeted since their pandemic peak and the initiatives above have yet to pay dividends. If they cannot turn around revenue growth, there will be even more drastic changes coming for the company.

The company stills remains optimistic, well, at least the CEO is. Barry delivered a great and candid quote in this quarter’s investor call:

“I've got a lot of tools in the toolbox. I mean, I don't mean to sound like one of those CEOs that's completely disconnected from the stock price because it's not lost on me that I walked in the door when it was 39 and it was hanging out about five bucks at the start of this call. But I have never been more optimistic. We're excited about the future of the business.”

Cash

Switching gears from revenue to profits, Peloton is still struggling with free cash flow. The company continues to lose money from its operations every quarter and is currently sitting on just $814 million.

After blowing through cash over the last two years, the company is now net cash negative (defined as cash and cash equivalents minus debt).

While we don’t think Peloton is facing immediate bankruptcy risk, it is safe to say they don’t have the healthiest of balance sheets.

The Magic Formula

Peloton’s future depends on the chart above. Peloton has pivoted from an equipment company to a subscription company with hopes their subscription business can subsidize their physical equipment sales in which Peloton loses money on every bike they sell.

The magic formula is that Peloton must make enough profit from its subscription fees to cover their operating expenses (headcount, office space, marketing costs). Peloton’s subscription gross margin is an impressive 67% which means for every dollar in membership fees they collect, they get to keep the majority of those fees as profit after deducting costs like instructor salaries and studio and streaming expenses.

The difference between subscription margin and operating expenses has been shrinking over time but the company still has work to do in order to fully close the gap.

Valuation

Peloton’s stock dropped 22% after this quarter’s earnings call. Investors are not optimistic and neither are we.

We cut our revenue projections for Peloton by almost 40% and downgraded Peloton’s long-term free cash flow margin from 12.6% to 6.4%. These were drastic changes to the model and reflect our declining confidence that Peloton will be able to turn it around.

We expected much larger progress with the business and there was none to be found. On top of that, the CEO’s comments on upcoming uncertainty came across as candid but also a major red flag for investors.

As such, we have updated our target price to $5.01 per share, right around where Peloton has traded the last few weeks.

Investment research disclaimer: the financial valuation methods, target prices, and model assumptions discussed above are for educational and informational purposes only and reflect only our views at the time of publishing. The information and/or strategies above should not be used to make investment decisions. Past results are not predictive of future performance and future investment proceeds are not risk free and cannot be guaranteed. We are not a registered investment advisor or broker and all investment decisions must be made independently of the educational research published here.