Earnings Analysis: Netflix Q3 2023

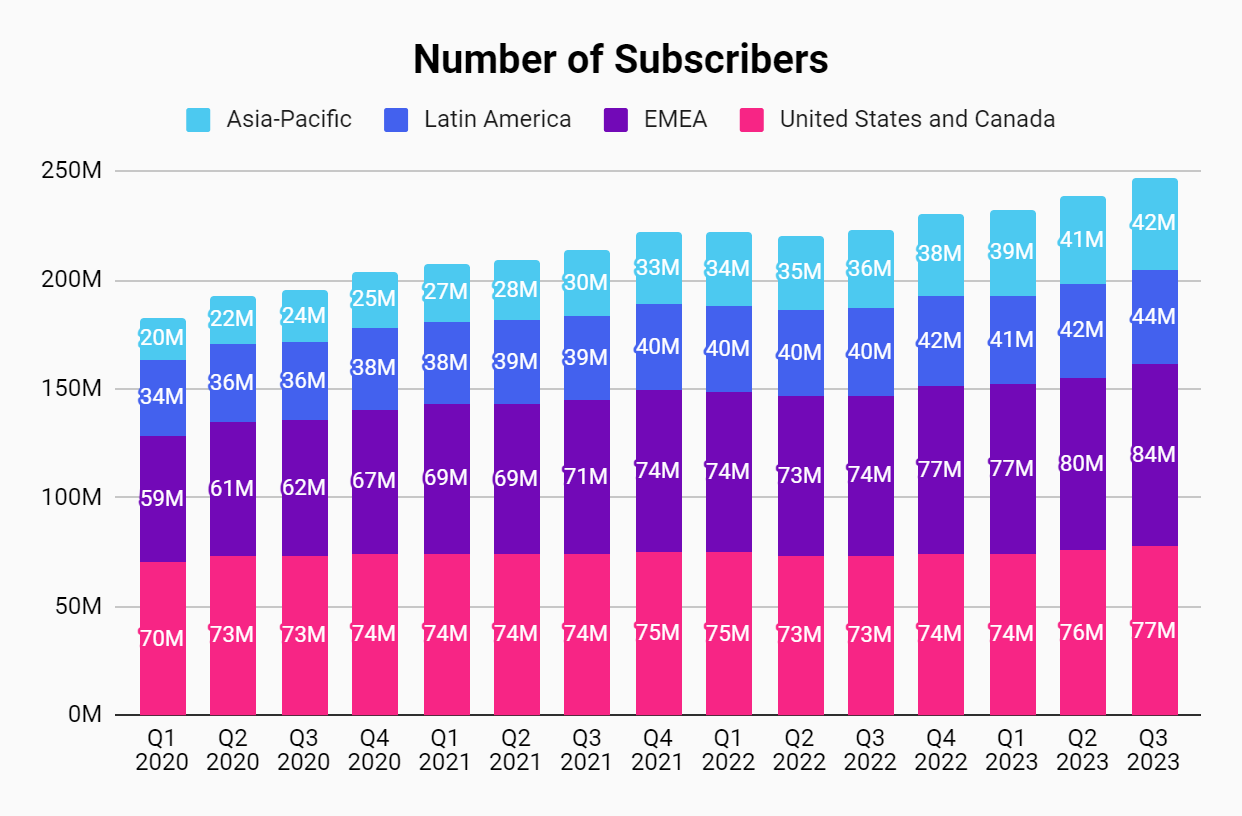

Summary: Netflix’s plan to stop account sharing is paying off financially. The company added 9 million new subscribers last quarter as the company approaches nearly 250 million subscribers globally.

Netflix has also carefully managed expenses and expects to grow operating margins in 2024. We have increased our price target for Netflix’s stock as the company continues to execute well and has impressed us with their ability to handle many large ongoing initiatives.

Previous target price: $197.95

New target price: $230.26

Current stock price: $401.77

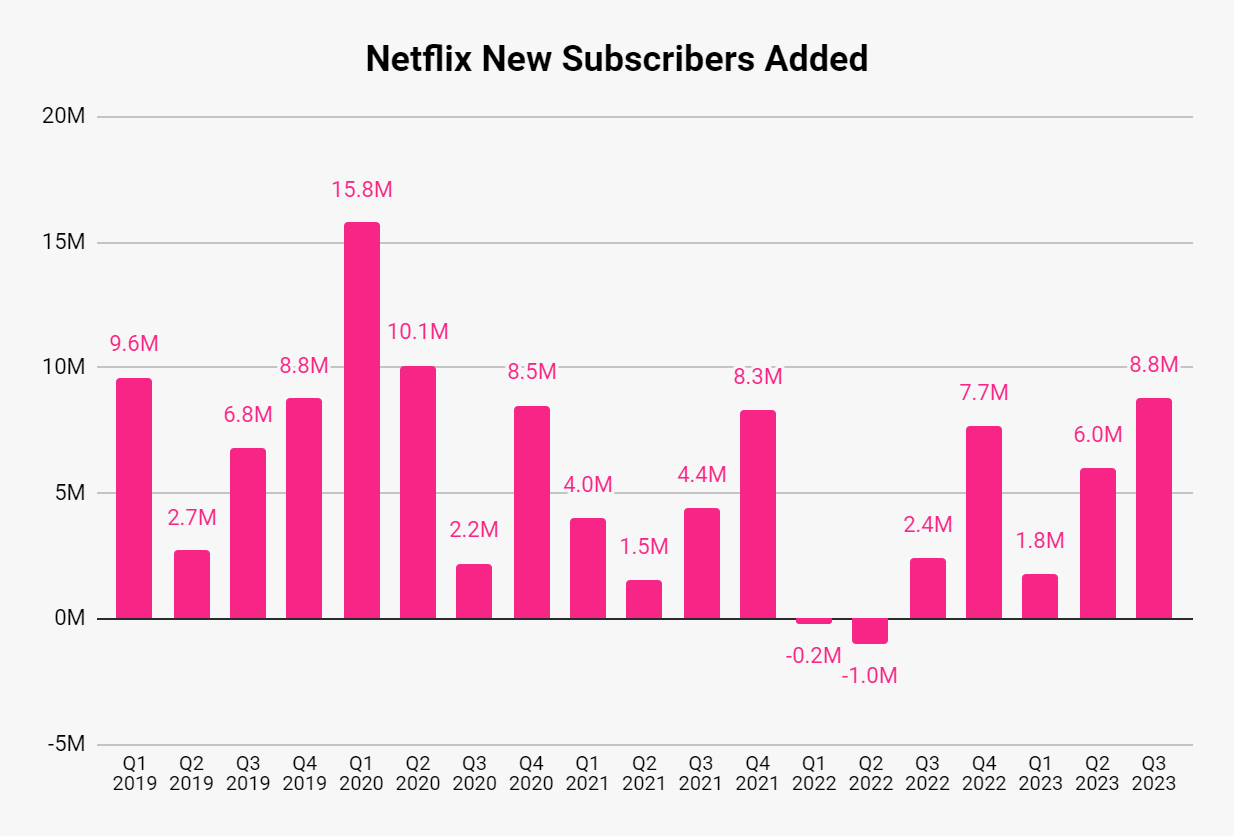

New Subscribers

As mentioned in the summary, Netflix has been able to convert people to new memberships after kicking them off shared accounts.

The company mentioned that their account sharing crackdown is still ongoing so we should expect subscriber growth to continue the next few quarters.

The password sharing crackdown has boosted membership in the US and EMEA, two regions that had become highly penetrated and saw little to negative growth in 2022. These two regions are important as they likely have large incremental margins due to higher membership costs and a large existing content library.

Revenue

The subscriber growth has restarted revenue growth at Netflix. After three consecutive quarters of low-single digit growth, revenue climbed 8% year-over-year last quarter.

On top of that, Netflix has recently stopped offering their basic ad-free tier for new subscribers and just raised prices on existing basic customers in order to convert more users to higher revenue tiers.

Remember that Netflix makes more money per subscriber on their lowest price ad-supported tier than their basic ad-free plan because of the ad revenue they collect outweighs the different in subscription price.

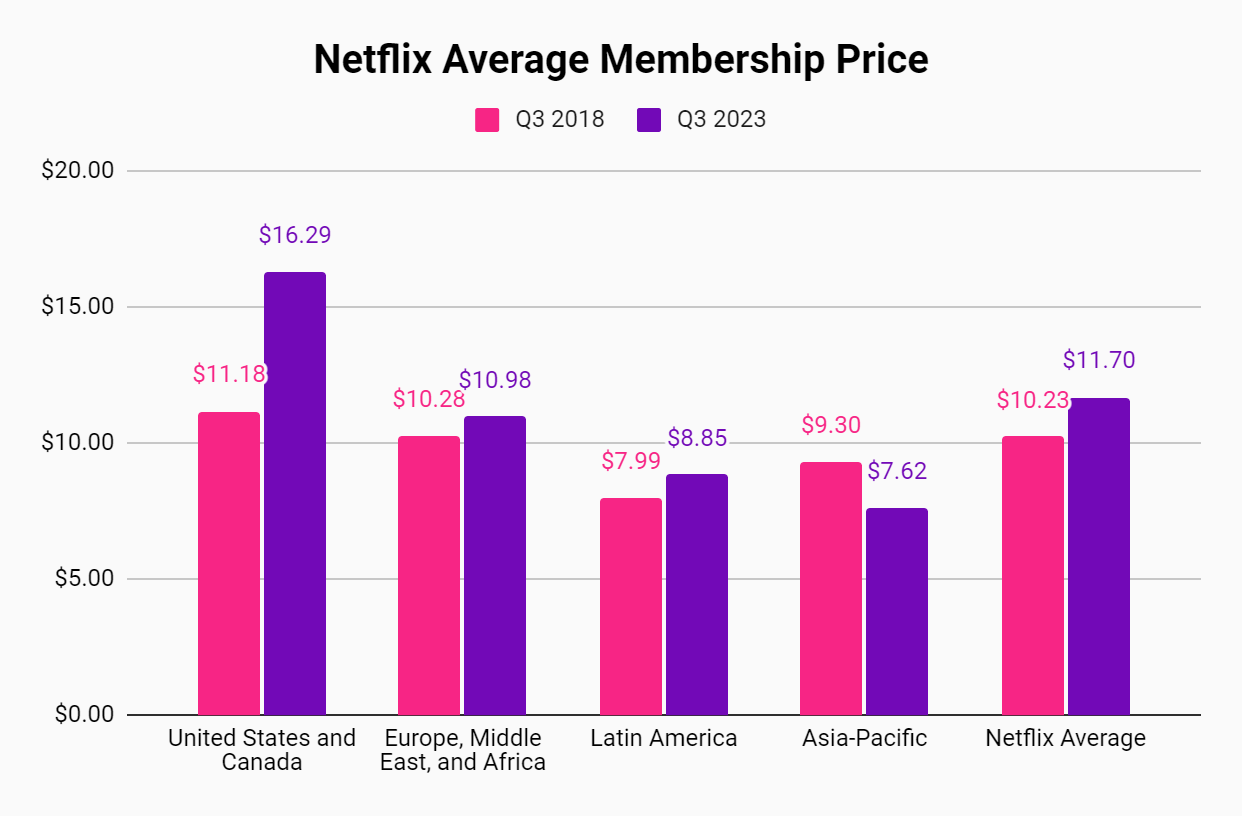

We can see the price increases in the US and Canada last year have boosted average revenue per subscriber to over $16 per month.

Taking a step back, we can see how much Netflix has raised prices in the US compared to other regions over the last five years.

Expenses

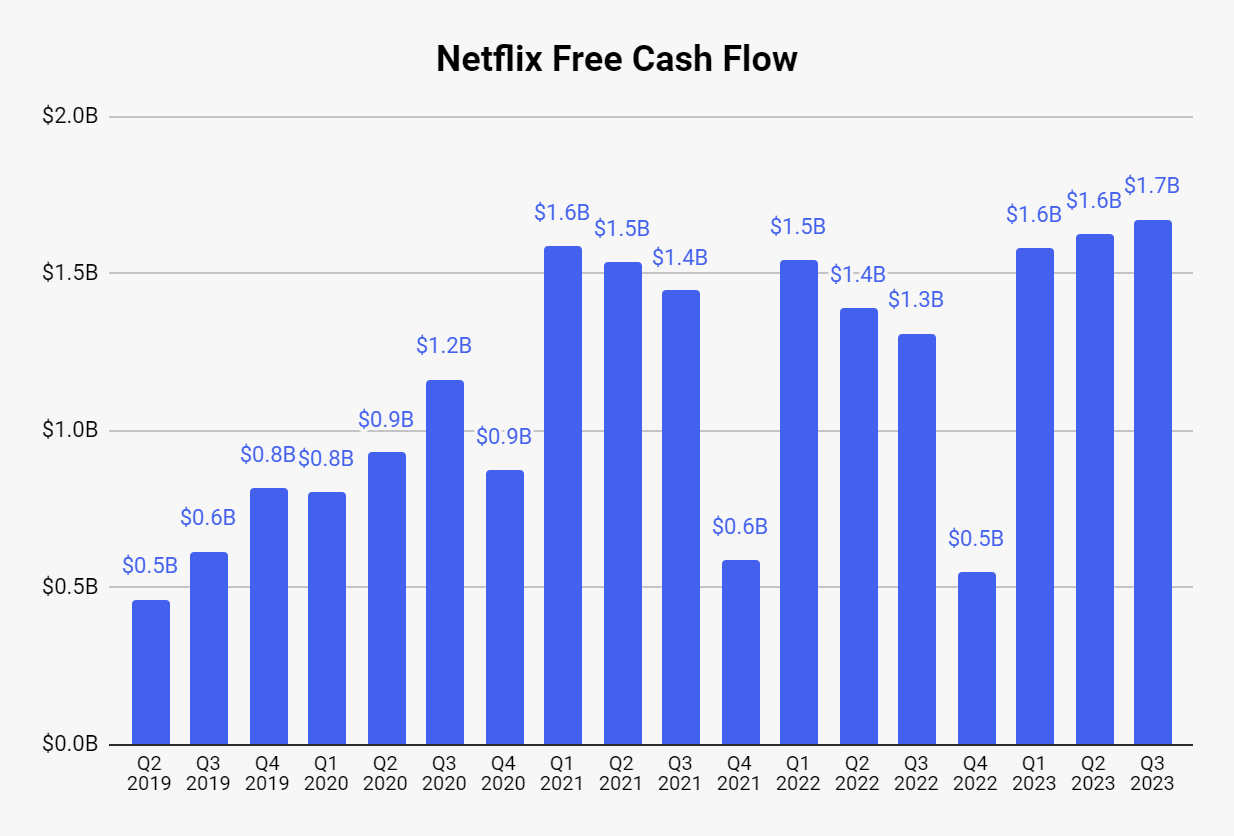

Another important takeaway from this quarter’s earnings call was Netflix management stating that they expect operating margins to expand from 20% this year to 22-23% in 2024.

This announcement was a surprise to investors because Netflix has stated they plan to increase content spend next year and it was unknown how that would affect’s Netflix’s margins.

Netflix has cut back on spending for new streaming content, partially attributed to the Hollywood strikes this year. Because the company amortized content spend, they are able to push out cost of revenue into the coming years which is why next year’s margins should improve despite an increase in content spend to about $17 billion in 2024.

On the operating expense side, the company has remained disciplined. Marketing spend has continued to fall after peaking in 2022 although G&A continues to rise as a percent of revenues.

Valuation

Our valuation is driven by our belief that Netflix will continue to generate the best content for years to come. As the competition cuts costs and struggles to become profitable, Netflix has nearly perfected the art of streaming as they know more than anyone on how to serve their customers with the best content.

The company has also executed several generational product changes very well amid a challenging environment in the entertainment industry. This gives us confidence Netflix can grow their gaming and ad-supported business to be the best in the industry which further increases the company’s upside.

Netflix’s customer focus and strong management team check our top two boxes for traits we invest in. So if you can stomach buying Netflix at its high current multiple, you can hopefully feel assurance that Netflix continues to pull further ahead from its competitors every day.

Investment research disclaimer: the financial valuation methods, target prices, and model assumptions discussed above are for educational and informational purposes only and reflect only our views at the time of publishing. The information and/or strategies above should not be used to make investment decisions. Past results are not predictive of future performance and future investment proceeds are not risk free and cannot be guaranteed. We are not a registered investment advisor or broker and all investment decisions must be made independently of the educational research published here.