Earnings Analysis: Google Q1 2023

Summary: Its an exciting time to be a Google shareholder. Our outlook on the company hasn’t changed much in the last six months:

The company’s Search, YouTube, and Cloud businesses should be just fine in the next 3-5 years after they weather the current slowdown in ad and cloud spending.

Google fell asleep at the wheel and lost their status as the leader in AI. OpenAI launched new products that people love while Google spent years on AI research and incremental improvements instead of breakthrough launches.

This has lit a fire under Google after years of complacency. The company has tremendous resources at their disposal (tens of thousands of the best engineers in the world and $150 billion in cash) and their management team is forced to go all-in on AI product launches or else they will likely be finding new jobs soon.

Our valuation is solely based on the factors above. The potential of Google’s AI capabilities is immense but the company has little to show for it so far due to years of poor management, starting with the CEO.

We have no idea where the AI race will go but we are ready for the show. Our Google target price remains pretty flat this quarter given the AI race has just begun and the benefits will not reach their full potential for years, or decades.

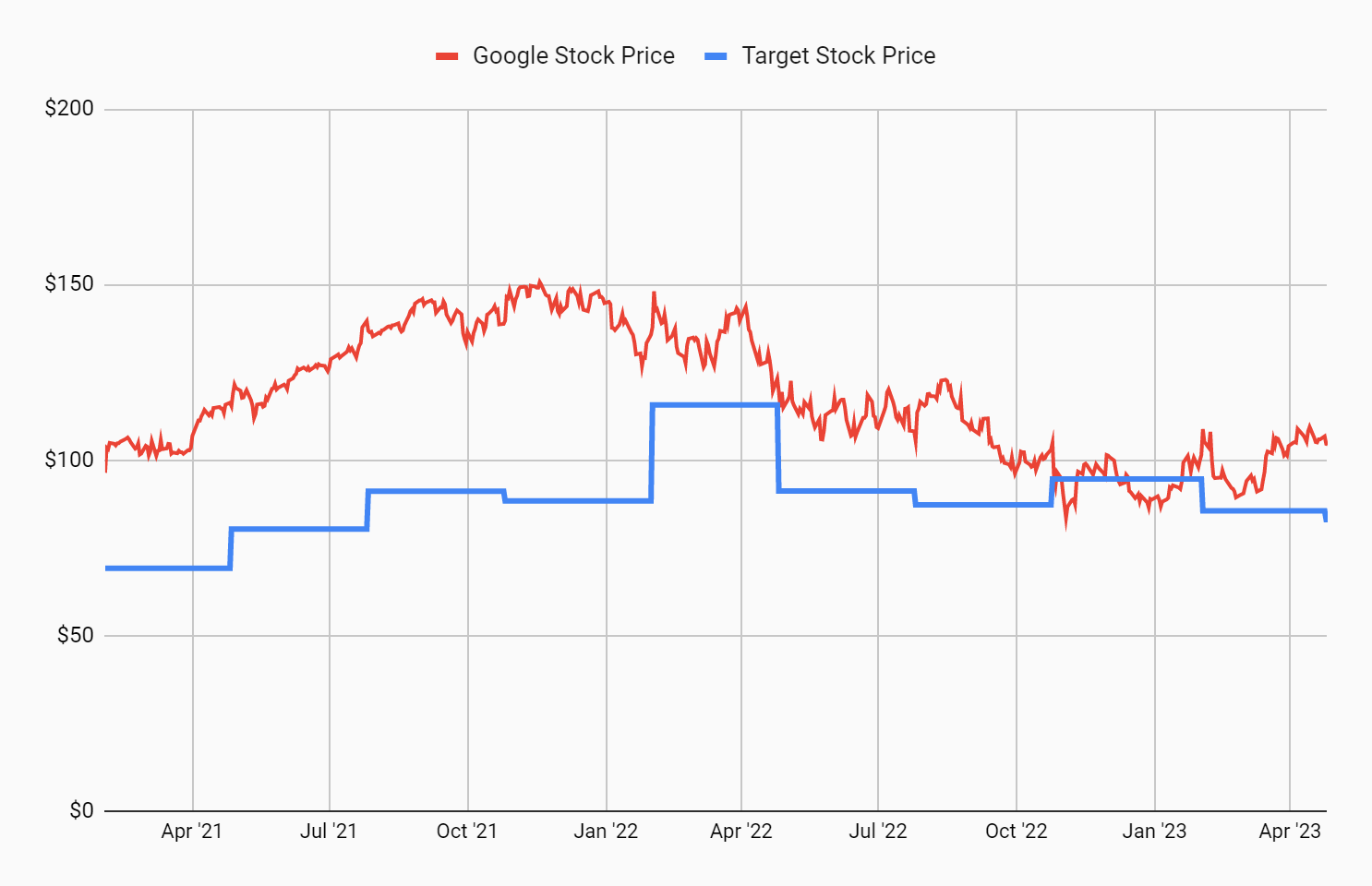

Previous target price: $85.57

New target price: $83.04

Current stock price: $103.71

Revenue

We’re not AI experts and no one can predict how much the new developments in AI will impact Google’s business, so let’s spend our time discussing the current state of the business.

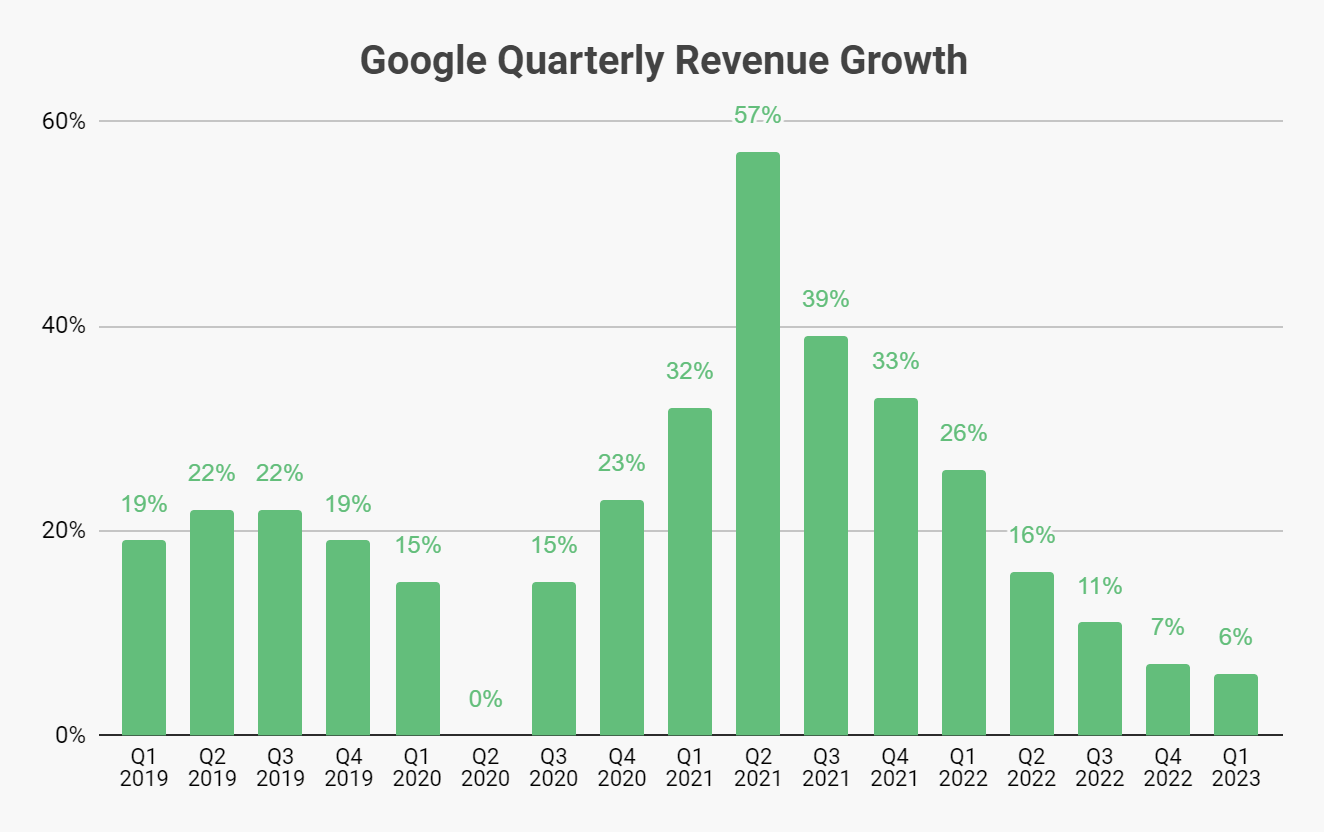

Google’s Q1 results were about what everyone expected. Slow revenue growth and decreasing operating income were again the story of this earnings release.

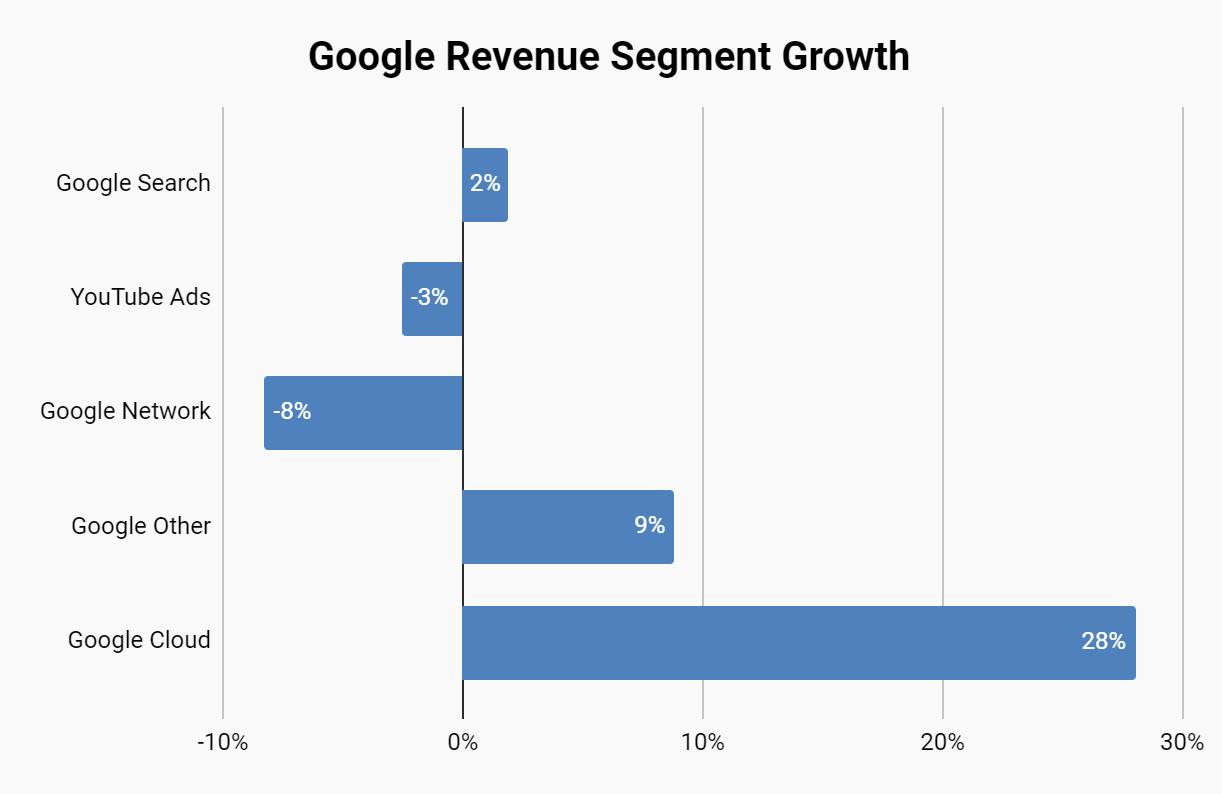

Google Cloud continues to grow at a healthy rate despite many companies pulling back on Cloud spend. It is important to note that Google Workspace is also included in the Google Cloud segment and is likely driving a decent portion of this growth.

Elsewhere, the company’s search business continues to get hit by companies pulling back on advertising spend. The ‘Google Other’ category is made up of Google Play commissions, YouTube subscription fees, and hardware sales. While they don’t break out each category, Google pixel continues to increase its market share in the US.

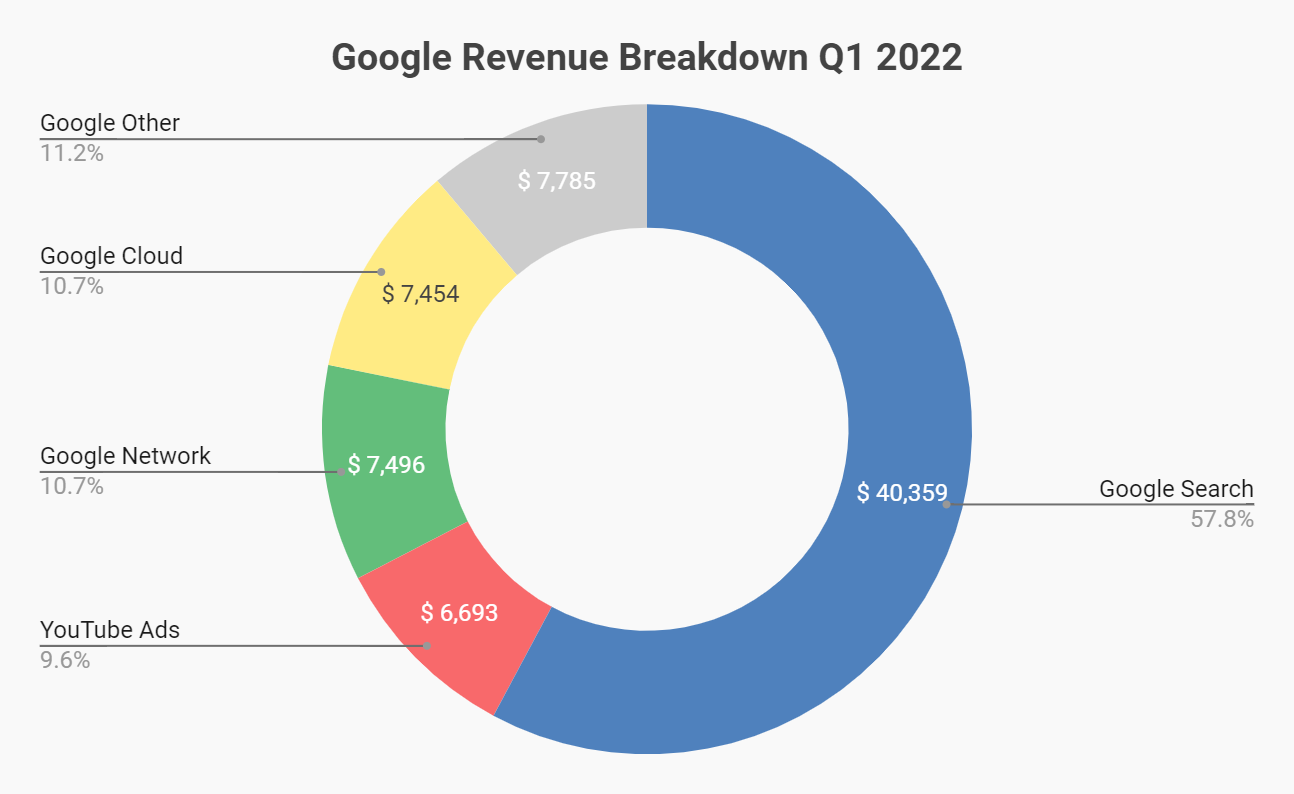

Zooming out we see that Google Search continues to make up over half of Google’s revenue. An important footnote is that this category also includes revenue from ads that are displayed on Google Maps, Gmail, and Google Play. Those three are likely each multi-billion dollar businesses which means Google is not as dependent on pure Google Search as we may believe.

Google’s management team also remains bullish on YouTube shorts as the company begins to monetize it. If TikTok bans were to continue, it could be a strong tailwind to Google’ business as advertisers look for more predictability and lower CACs in their advertising campaigns.

Expenses

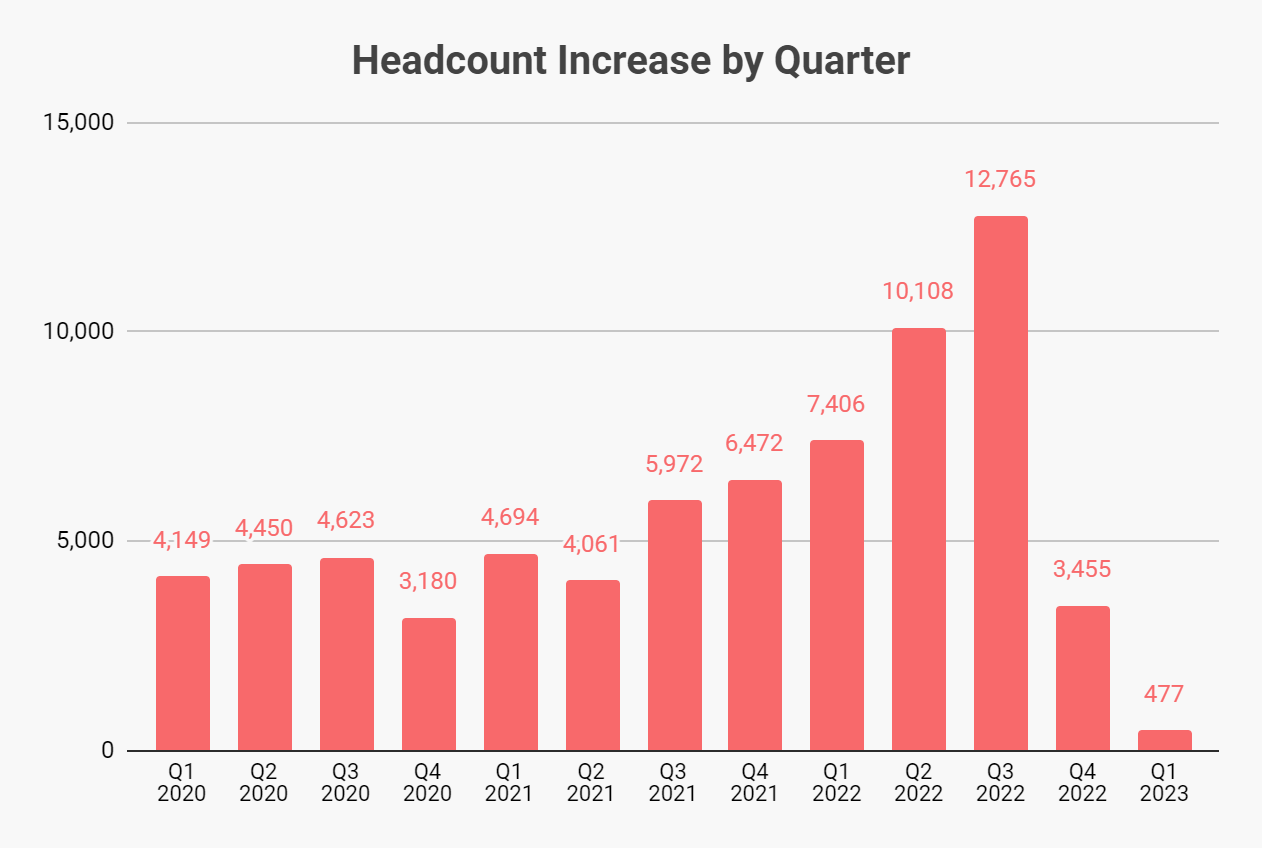

Talk about poor management. How did Google’s executive team think that hiring 13,000 people per quarter was sustainable?

Google laid off over 10,000 people in January and that won’t be reflected until next quarter’s earnings release due to rules on how severance affects official employee counts.

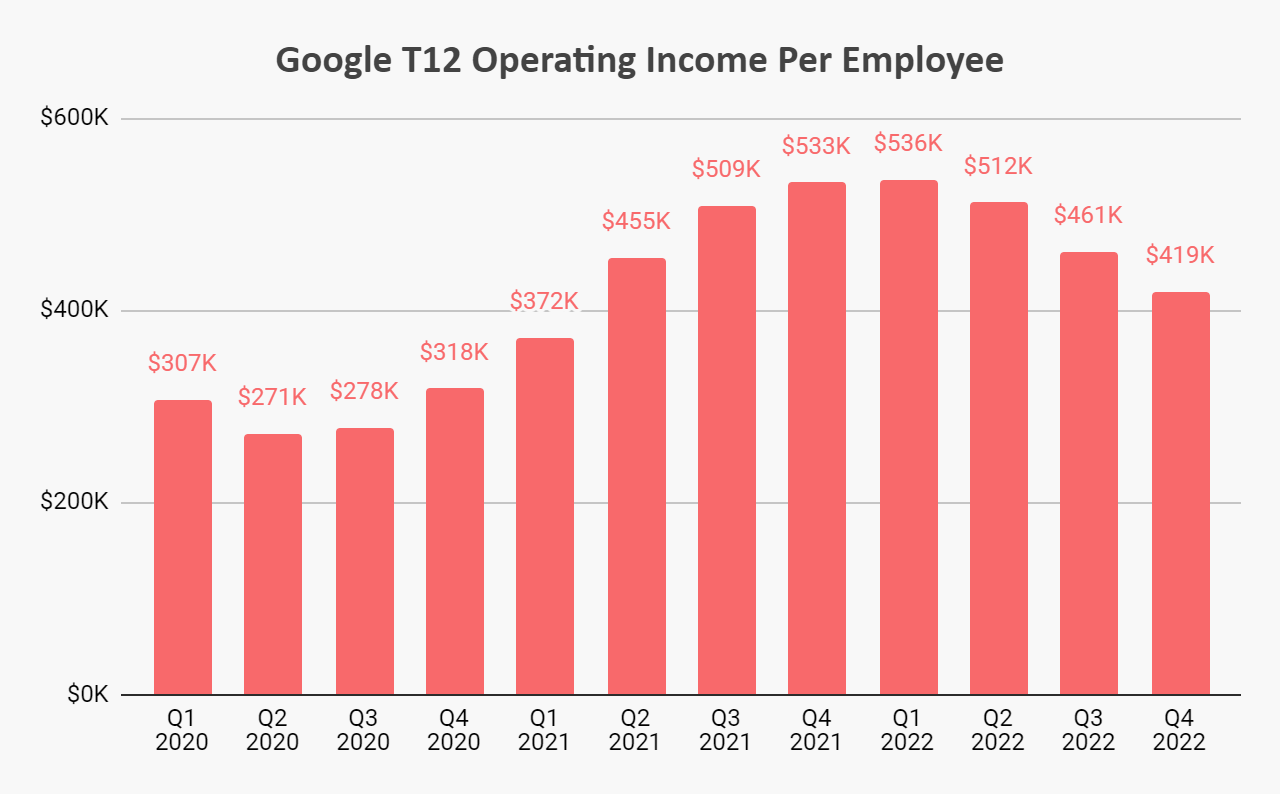

While Google investors may think the sky is falling, the company is still well above pre-pandemic levels in terms of profit per employee. On an annualized basis, Google still makes $400,000 in operating profit per employee, which is more than many companies make in revenue per employee.

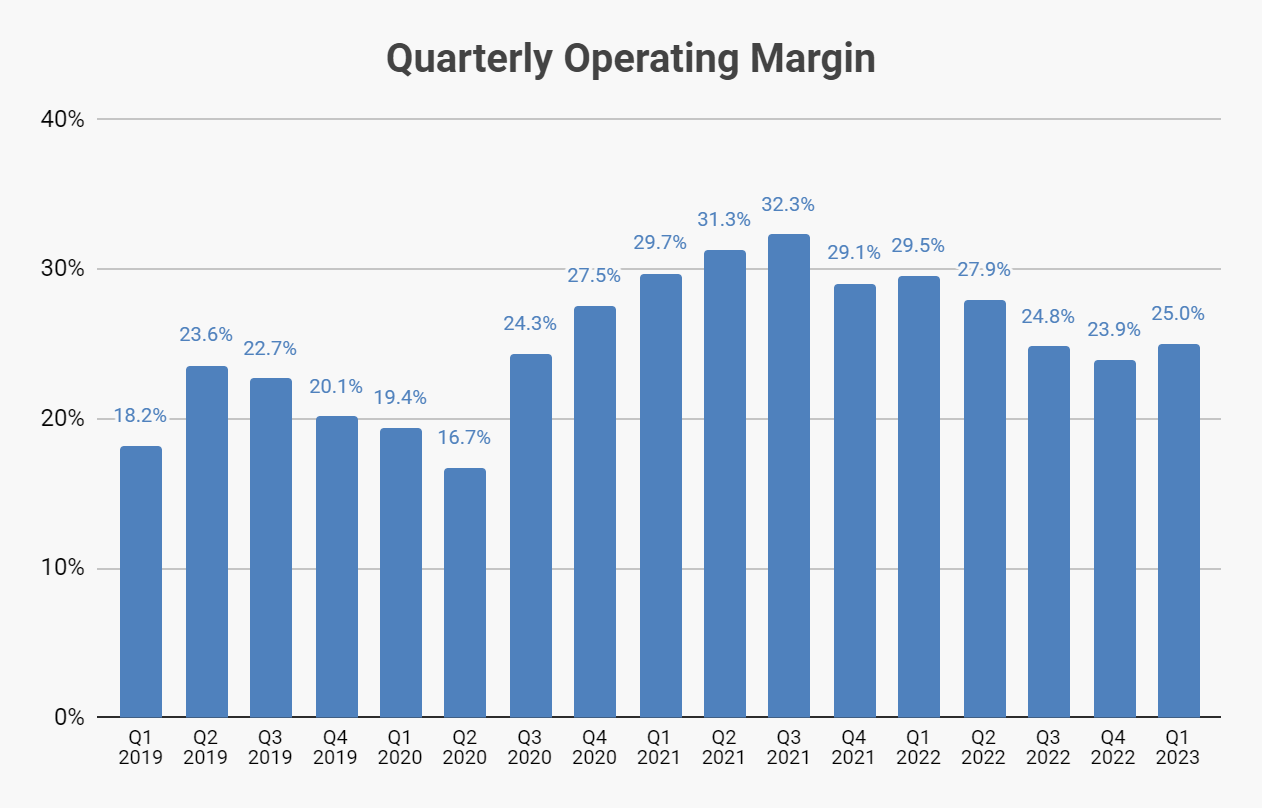

Additionally, even with costs getting out of control, the company’s operating margins also remain above pre-pandemic levels. If the company continues to grow while keeping expenses flat, this should eventually start to rise again in the second half of this year.

Valuation

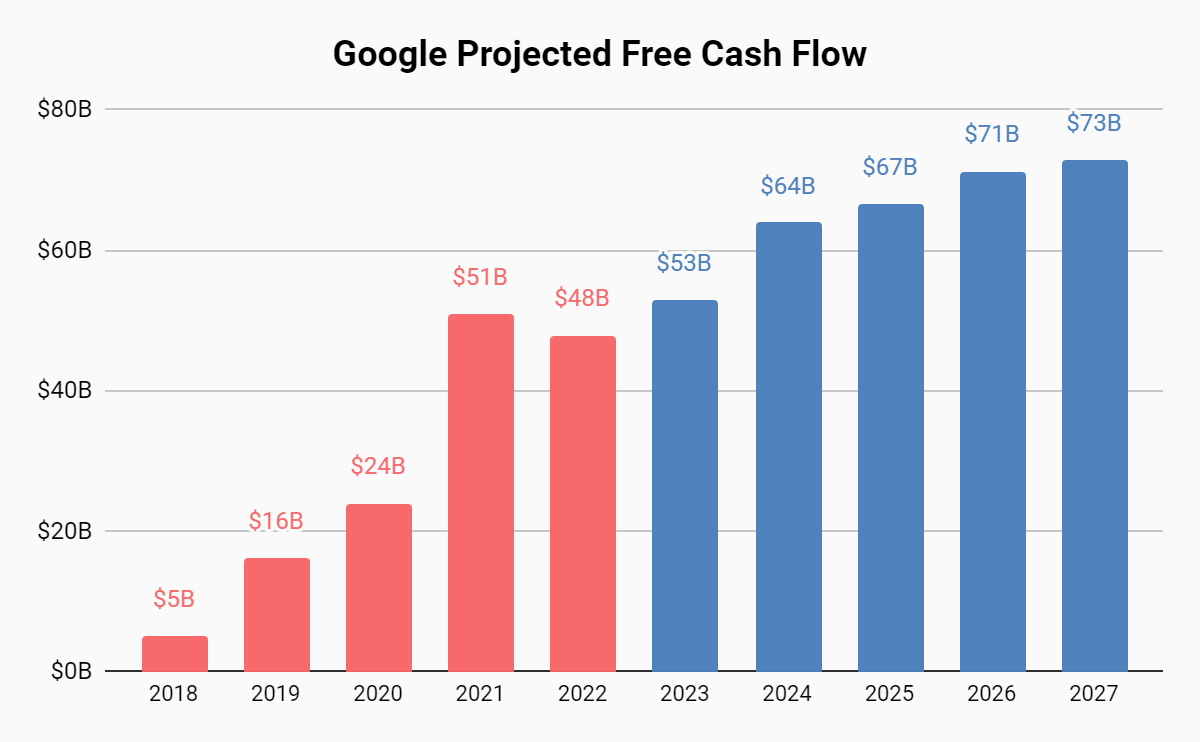

We are forecasting that Google will be able to grow total revenue at a high single digit rate over the next few years. On top of this, most companies have recently learned what expense management is which will greatly benefit the bottom line.

At this point, we remain too bearish on Google’s management team to recommend Google’s stock at this price point. Don’t get us wrong, Google could nail their investments in AI and become the most profitable company in the world. That world is years away but we will continue to monitor any developments as they happen.

Investment research disclaimer: the financial valuation methods, target prices, and model assumptions discussed above are for educational and informational purposes only and reflect only our views at the time of publishing. The information and/or strategies above should not be used to make investment decisions. Past results are not predictive of future performance and future investment proceeds are not risk free and cannot be guaranteed. We are not a registered investment advisor or broker and all investment decisions must be made independently of the educational research published here.