Earnings Analysis: Amazon Q3 2023

Summary: Amazon just recorded their highest operating profit quarter in company history, and they’re just getting started.

Amazon showed their plan of warehouse optimization, cost cutting, and leaning into advertising, Prime Video, and AWS is paying off handsomely. We have raised our price target to reflect Amazon’s strong execution and continued customer obsession.

Previous target price: $128.91

New target price: $136.78

Current stock price: $127.74

One year ago…

In order to understand where Amazon is today, we have to look back to where they were this time last year.

In Q3 2022, Amazon reported negative $3.7 billion in free cash flow, one of their worst quarterly losses ever, due to the following problems:

Slowing growth: Amazon grew revenue “only” 9% in 2022, down from 22% in 2021 and 38% in 2020. The 9% growth in 2022 marked the first year ever that Amazon did not grow annual revenue by 10%.

Over-capacity: The company grew their spending on capital expenditures 5x from 2019 to 2022 in order to build new warehouses, delivery trucks, and data centers to meet the skyrocketing demand they faced in the pandemic. With slowing growth however, the company realized they had grown too fast.

Over-hiring: Amazon, like almost every company in 2021 and 2022, hired too many employees. Amazon had 340,000 employees in 2016 which had grown to 1,500,000 employees by mid-2022. While most of their employees work in their fulfillment centers, the number of corporate employees also skyrocketed during this period. As such, the company’s operating margin fell 75% in just six quarters from Q1 2021 to Q3 2022.

Investors concern about the free cash flow losses sent the stock down 54% from its 2021 high to the end of 2022.

For some added context, this was all happening in Andy Jassy’s first year as CEO after Jeff Bezos stepped down in July 2021. While many investors were not blaming Jassy directly for Amazon’s struggles, questions were being asked about Amazon’s future without Bezos.

So how was Jassy planning to turn Amazon around?

The Plan

Amazon’s plan was simply massive cost cutting through headcount reductions and optimizations while supporting its profitable business lines:

Expand highly profitable business lines: Amazon continues to grow AWS and their advertising business by double digits each quarter. What is unique about these business lines are that they are highly profitable. AWS now has 30% operating margins and the advertising business could have 50%+ operating margins.

Layoffs: Amazon has laid off 27,000 corporate employees across the company in the last 12 months, which has saved the company billions in headcount costs.

Warehouse optimization: We mentioned that Amazon found themselves with too much warehouse space last year. The company began selling off excess warehouse space and began one of Amazon’s most successful projects ever - the regional warehouse network.

Amazon has discussed the regional warehouse network project at length in their earnings calls, but essentially Amazon divided their US fulfillment network into distinct regions, where each region is responsible for holding as much unique inventory as possible.

This allows products to be closer to the consumer which improves delivery speed and reduces costs as Amazon is less reliant on shipping products across the country to meet delivery windows.

Now that we have this context, let’s take a deep dive into Amazon’s quarter.

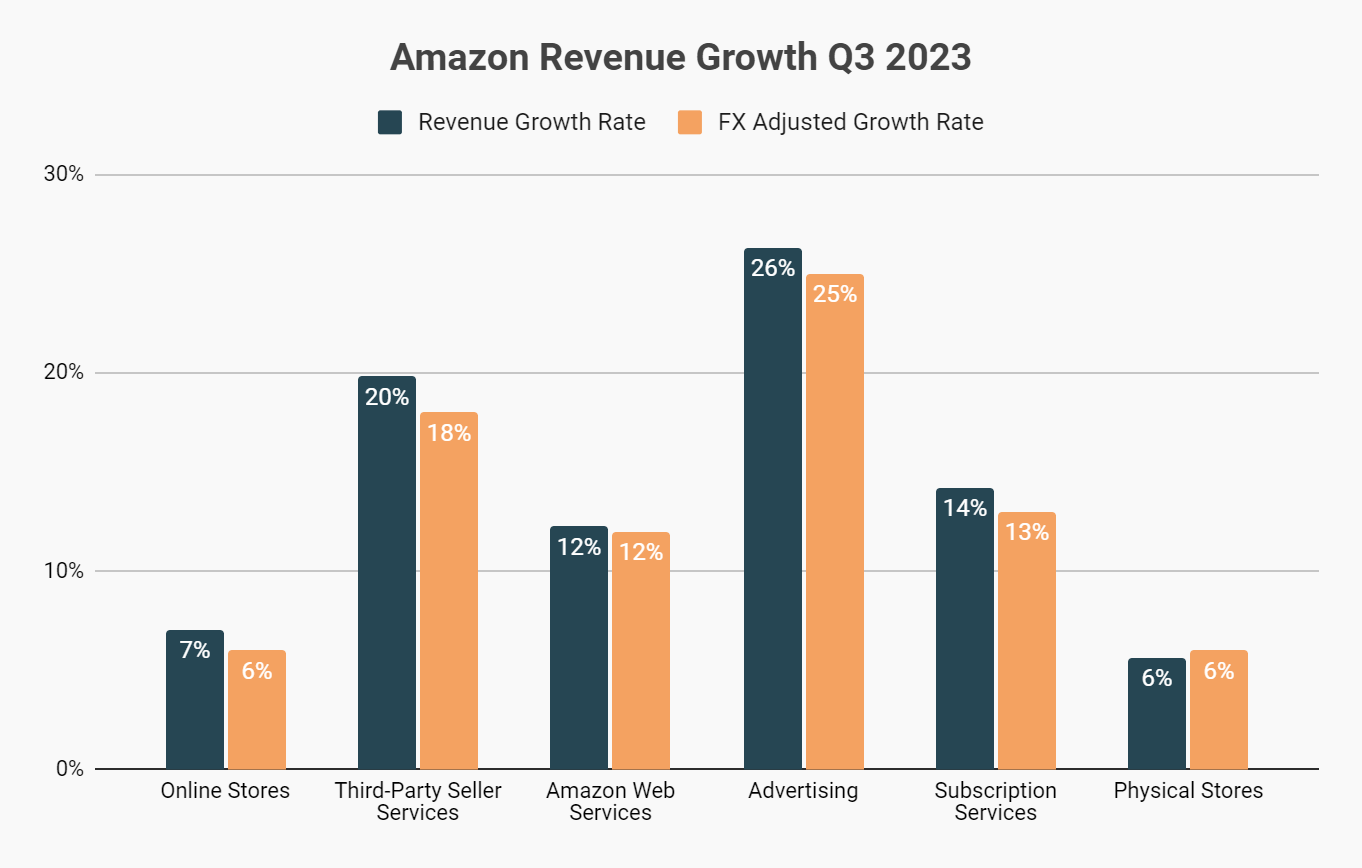

Revenue Growth

Good news - Amazon’s revenue growth has accelerated each of the last four quarters. Even better news - the revenue grow is increasingly concentrated in its highly profitable business segments.

Third-part seller services, AWS, advertising, and subscription services drive the vast majority of Amazon’s profits and all four segments are growing by double digits.

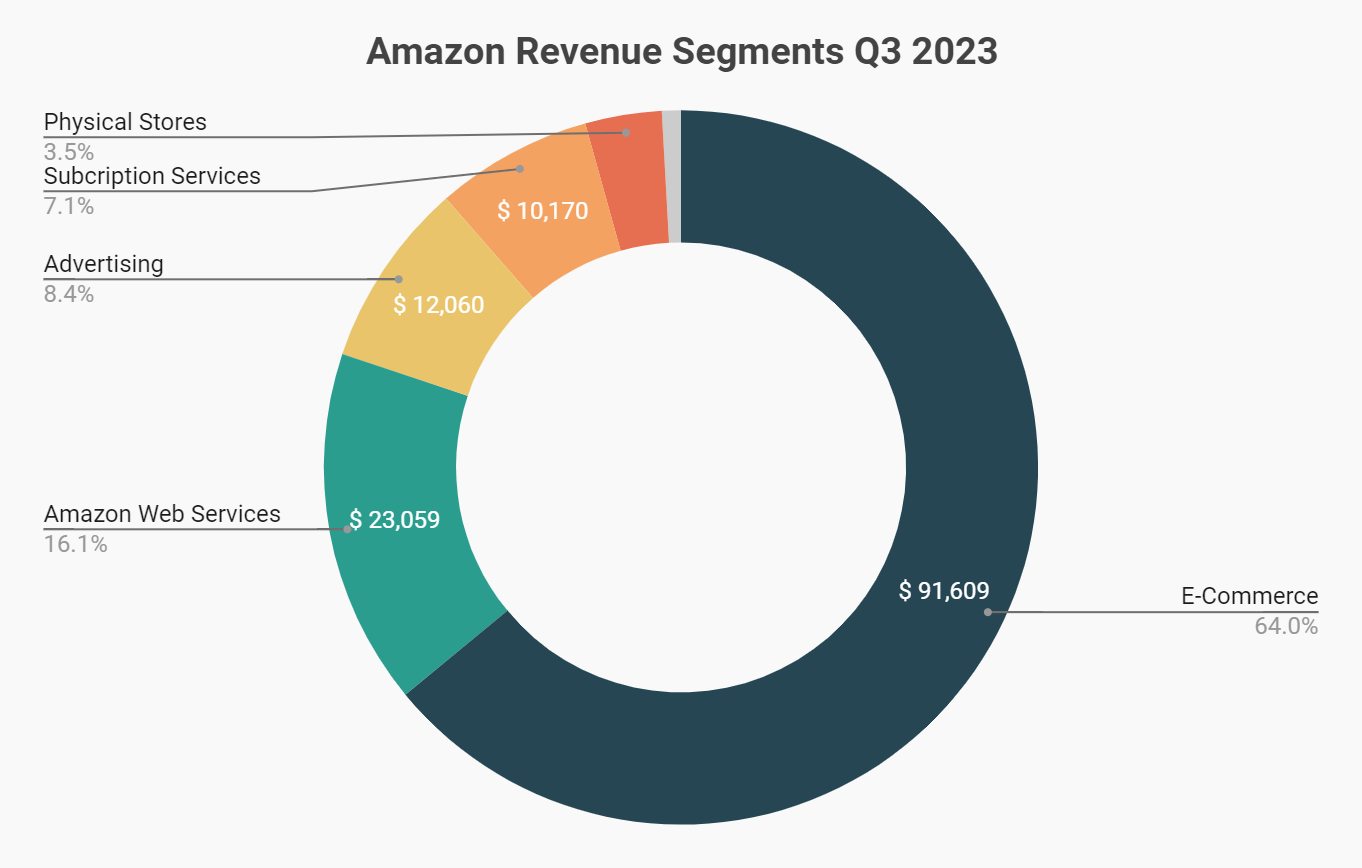

This growth has helped Amazon diversify away from ecommerce as AWS now makes up 16% of revenue and advertising 8% of revenue and growing.

Amazon continues to build a powerful business model by having highly profitable segments drive profits while the company continues to expand retail market share with low prices.

As Amazon grows its profit making businesses, the company’s gross margin has expanded:

If this chart doesn’t impress you, here is why its important: every 100 basis point improvement in gross margin equals an extra $5 billion in profit for Amazon.

Step 1 of Amazon’s turnaround plan? Check.

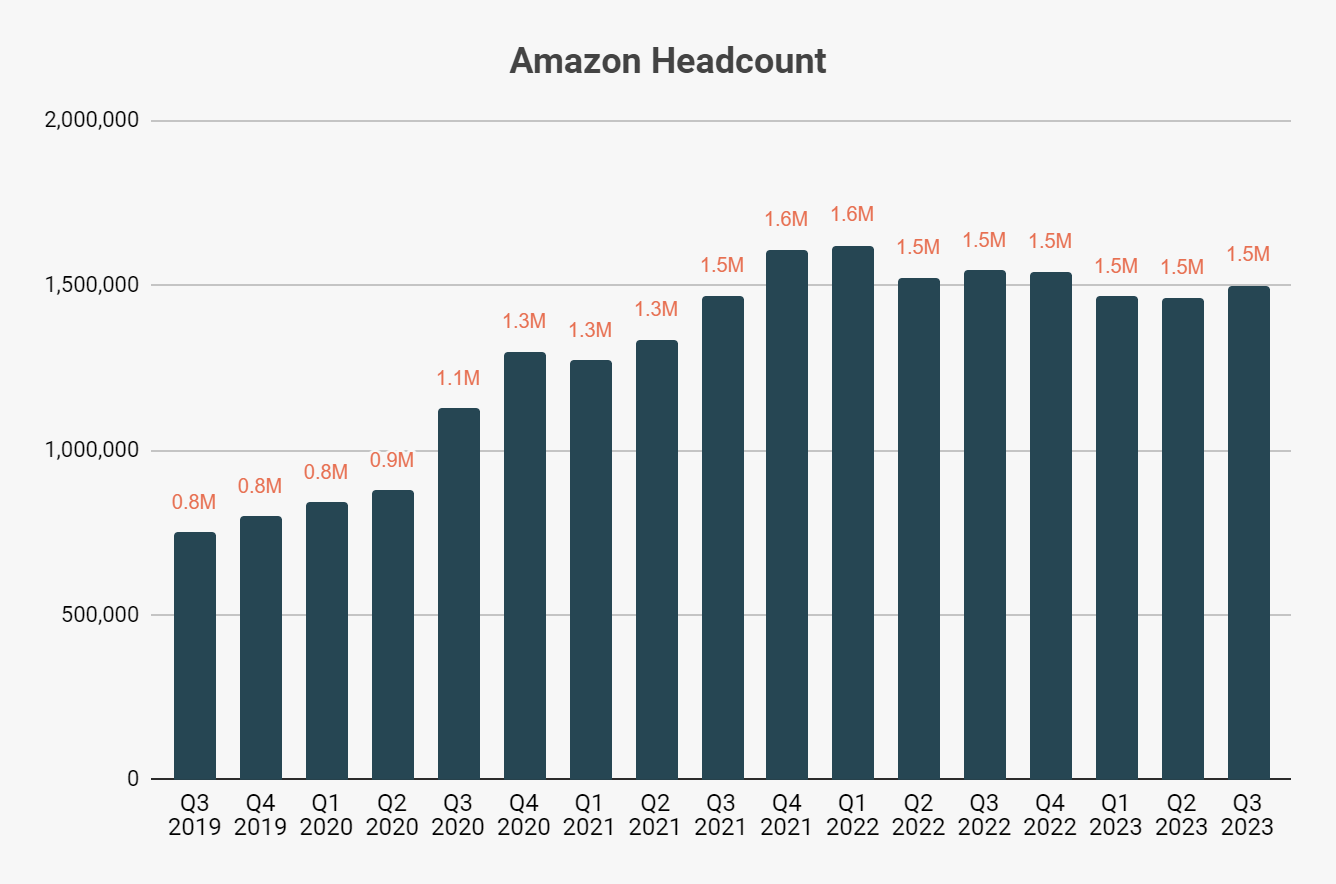

Headcount Growth

Amazon has moderated headcount growth even as revenue continues to grow.

The chart outlines the hiring frenzy Amazon went on to staff fulfillment centers around the world as the pandemic took off in 2020. Headcount peaked in Q1 2022 until they started to scale back warehouse usage and slow corporate hiring.

Revenue growth + headcount reductions = more profits. Step 2 of turnaround plan? Check.

Warehouse Utilization

To put into perspective just how much warehouse space Amazon built recently, Amazon doubled their fulfillment network square footage in just over two years.

So it took 26 years for Amazon to build their 300 million square foot network and added another 300 million square feet in 2.5 years.

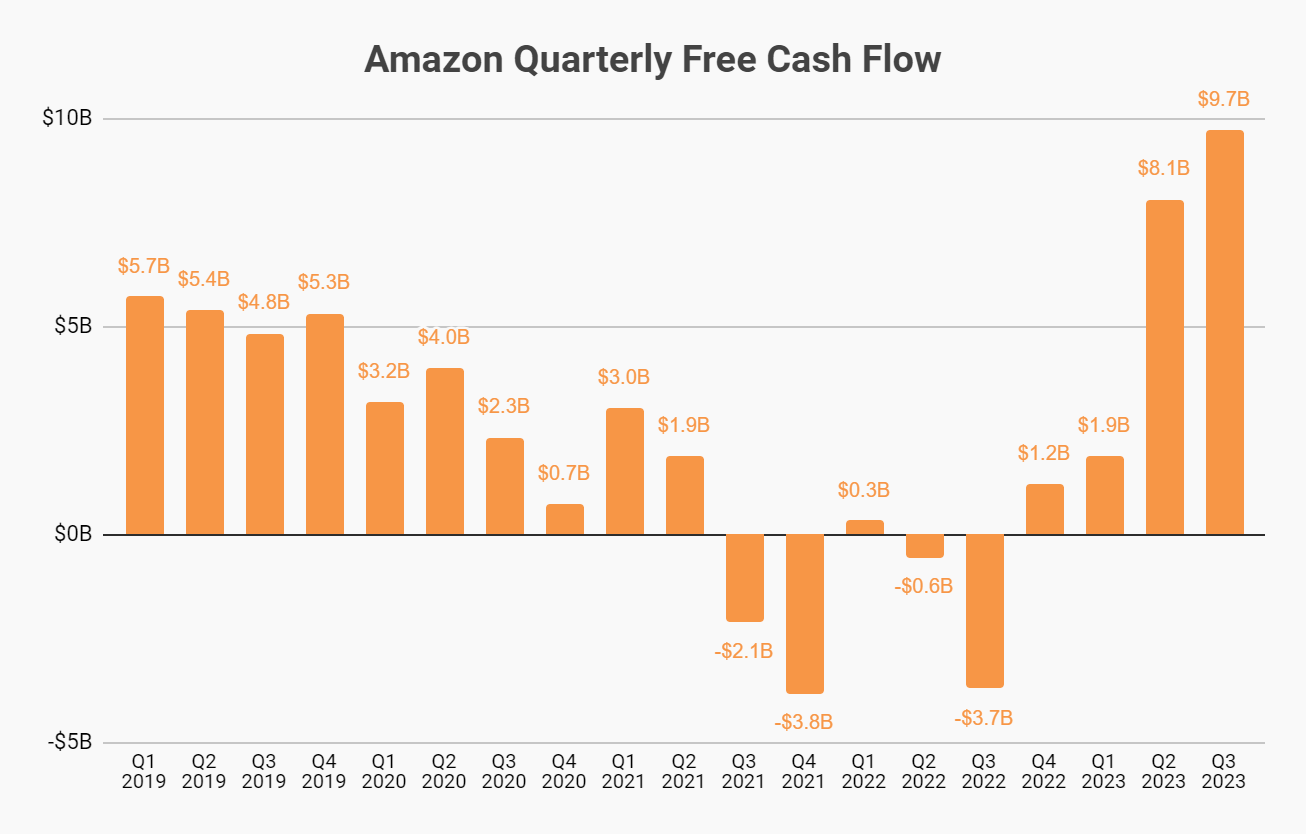

The warehouse expansion plan was costly. Construction costs and equipment purchases show up as capital expenditures on the cash flow statement.

If we examine Amazon’s cash flow statement over the years, we see a massive expansion of capex. Capex costs need to be paid immediately with cash and the depreciation benefit is recognized over time.

Jassy’s plan to sell off and reduce warehouse space resulted in less capex spending which has benefited Amazon’s free cash flow immensely. Step 3? Check.

The Results

We have seen that Jassy and Amazon have nailed all three points to their turnaround plan. The results are certainly showing their progress:

Amazon logged their highest free cash flow quarter ever, just one year from recording one of their worst quarters ever. The turnaround is really one for the history books (with Meta’s recent turnaround also being quite impressive).

What gives investors excitement is that the turnaround is still ongoing. The company continues to keep operating costs and capex low which will allow for Amazon to hit record cash flow for years.

Earnings Call

This was one of the most well executed earnings calls we have listened to this year. If you remember earlier this year, Amazon’s stock started plummeting during their Q1 earnings call as the company hinted that AWS growth was slowing. Amazon learned from this and delivered a strong call that focused on the massive revenue potential ahead for AWS and Amazon as a whole.

Here are are favorite quotes from this quarter’s call:

AWS Revenue Growth

“You look at the very substantial gigantic new generative AI opportunity, which I believe will be tens of billions of dollars of revenue for AWS over the next several years, I think we have a unique and broad approach that's really resonating with customers.”

“It's hard to compare and do the math across different players because not everyone discloses them clearly. But as far as we can tell, that also looks like the most absolute growth of any of the players out there.”

“And then we have a $92 billion revenue run rate business where 90% of the global IT spend still resides on premises. And if you believe like we do, that equation is going to flip. There's a lot more there for us.”

Fulfillment Network Optimization

“Our move earlier this year from a single national fulfillment network in the U.S. to eight distinct regions represented one of the most significant changes to our fulfillment network in our history.”

“We remain on pace to deliver the fastest delivery speeds for Prime customers in our 29-year history.”

“When customers are getting items as quickly and conveniently as they are now from Amazon, they're going to consider us more frequently for more of their shopping needs.”

Miscellaneous

“In our established countries, U.K., Germany, Japan, France, those countries are profitable and have been profitable. And we continue to work on price selection and convenience.”

“During the quarter, we held our biggest Prime Day event ever with Prime members purchasing more than 375 million items worldwide and saving more than $2.5 billion on millions of deals across the Amazon store.”

“Take "Thursday Night Football," which is we're in our second season of "Thursday Night Football," and off to a great start, the ratings are 25% higher than they were a year ago through six weeks.”

Valuation

The turnaround plan execution, strong growth, and the company’s customer obsession gave us confidence to raise our price target to $136.78.

For our newer readers, our price targets are discounted heavily and therefore are conservative compared to other analyst ratings. All you need to know is that we, and many analysts, are excited to see how far Amazon can take free cash flow. There is no limit in sight right now.

Investment research disclaimer: the financial valuation methods, target prices, and model assumptions discussed above are for educational and informational purposes only and reflect only our views at the time of publishing. The information and/or strategies above should not be used to make investment decisions. Past results are not predictive of future performance and future investment proceeds are not risk free and cannot be guaranteed. We are not a registered investment advisor or broker and all investment decisions must be made independently of the educational research published here.