Earnings Analysis: Amazon Q2 2023

Summary: Amazon blew out earnings this quarter as revenue growth outpaced expectations and the cost cutting boosted the bottom line.

Despite the stock rising 10% after earnings, we cut our price target by 4% as we are forecasting higher than expected expenses in the next several years.

Previous price target: $ 134.75

New price target: $ 128.91

Current stock price: $ 139.57

Free Cash Flow

Amazon called their shot and they absolutely nailed it this quarter. Here is what Amazon was telling investors the past year:

Revenue growth will remain strong, driven by third party merchants, subscriptions, and advertising even as retail and AWS growth hits economic headwinds.

Expenses will be managed through layoffs and optimizing the warehouse fulfillment network.

Capital expenditure spending will fall as the company built up its warehouse network in 2020 and 2021 allowing the company to spend significantly less on new warehouses in the coming years.

And that is exactly how it the story is playing out right now as Amazon recorded its highest ever free cash flow quarter. Let’s break down each component above in more detail.

Revenue

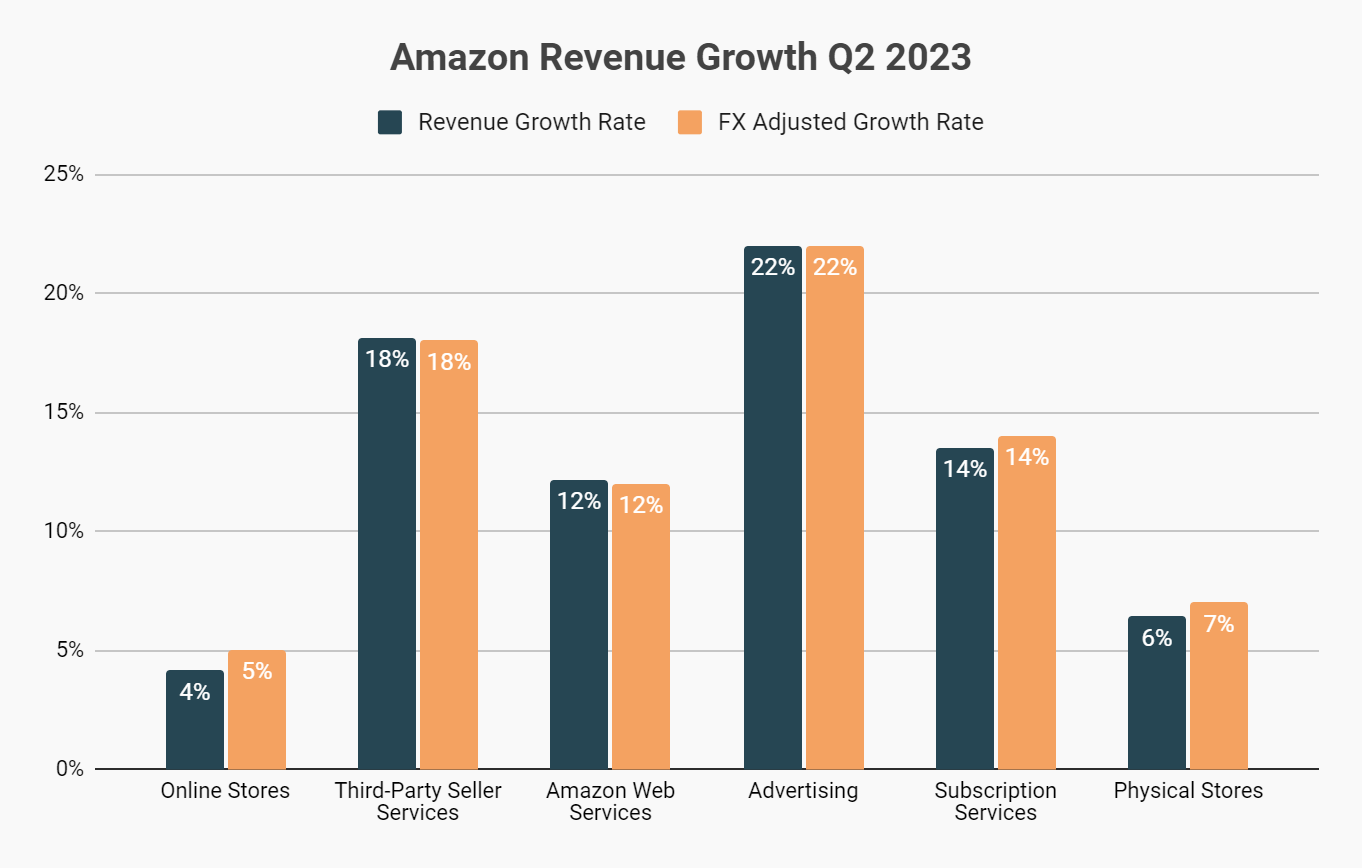

Amazon has built an incredibly well diversified business that deserves more recognition. The benefits of their business model diversification was on fully display this quarter.

Online stores and AWS, two of Amazon’s three largest segments, have seen revenue growth decelerate faster than other segments due to various economic reasons. While this would be catastrophic for most companies, Amazon has seen other segments like advertising pick up the slack.

Amazon’s advertising business continues to break records as the company scales their highly profitable ad business by showing more high quality ads across its website. This led to Amazon growing total revenue by 10.8% this quarter, only its second double digit revenue growth quarter in the last seven quarters.

Expenses

After several rounds of layoffs and cost cutting Amazon has finally returned back to 2021 profitability levels. We expect operating income to continue to grow in the foreseeable future as we forecast that revenue growth will outpace operating expense growth.

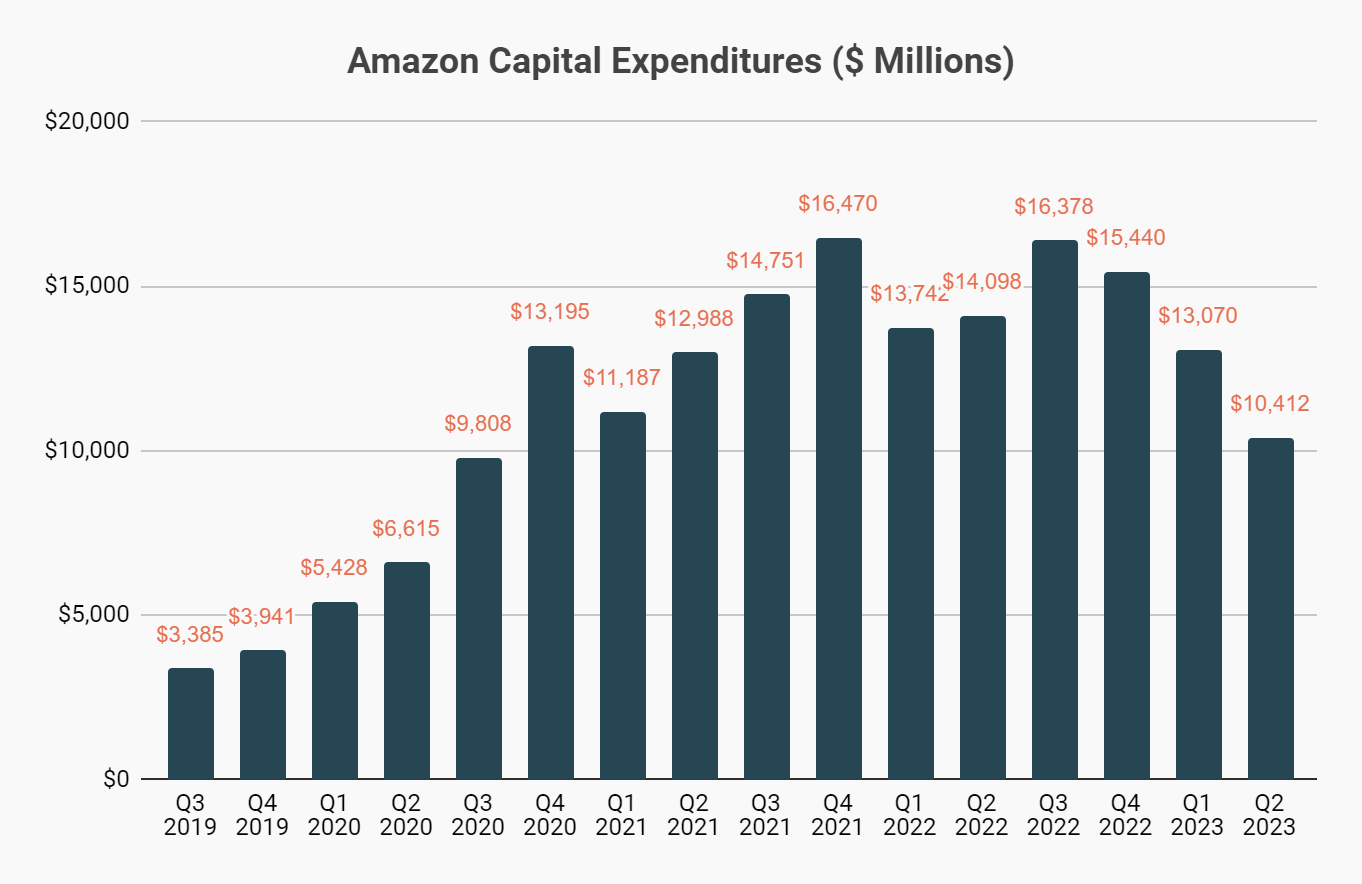

Capital Expenditures

The third driver of Amazon’s free cash flow growth has been a reduction in capital expenditures.

As Amazon’s revenue was growing 40% in the first few quarters in the pandemic, they need to invest heavily in more warehouse space in order to meet the surge in customer demand. The spending on new warehouses and data centers boosted Amazon’s capex spend from $13 billion in 2019 to $55 billion in 2021. That scale of capex growth is practically inconceivable.

The good news is that the upfront investment is now paying off as the company has sufficient warehouse capacity and can cut capex costs. Not only are capital expenditures going down, but depreciation expense is increasing as the company expenses all the recent capex spend which further boosts free cash flow.

Our Main Concern

So Amazon had a great quarter and everything is going according to management’s plan, so why did we lower our target price?

We are seeing a very clear shift in Amazon’s business model forming over the past two years that will pressure the bottom line. As Amazon grows revenue in its higher margin businesses (advertising, subscriptions, and AWS) faster than its low margin businesses (online stores and physical stores), we will see Amazon’s gross margins improve. However, this comes with a tradeoff of higher operating expenses to maintain these services.

We can see this trend in the chart above. Amazon’s gross margins as a percentage of revenue has dropped from 57.5% to 51.6% in the last eight quarters which is great news for the company and investors. While that is a great improvement, operating expenses have increased even faster, from 34.3% of revenue to 42.7% of revenue.

A great example of this is Amazon’s advertising business. The business is a high gross margin business because their are minimal costs involved in fulfilling ads on Amazon’s website. The vast majority of the costs related to the business are costs like the engineers who have to build the ad network and the salespeople who work with companies to sell the ads, which fall under operating expense line items.

This chart breaks down Amazon’s spending for each operating expense category.

Our main concern is with the technology and content bucket which we see has increased from 10% of revenue in Q4 2020 all the way to 16% of revenue this past quarter.

Amazon is clearly investing heavily into content for Amazon Prime Video as they now own the steaming rights for Thursday Night Football and have spent billions on developing original content.

On top of that, Amazon is still investing heavily in engineering talent for the business which will further increase operating costs and continues to be one of the highest spending companies in the world on advertising.

If Amazon is to justify its current valuation, they will need to keep operating expenses in check.

Valuation

Our investment thesis in Amazon still stands: we believe Amazon will grow free cash flow significantly by continuing to grow its high margins business segments while reducing operating expenses through layoffs and optimizations.

The only change this quarter was we increased forecasted operating expenses which slightly reduced the bottom line.

At the time of writing, Amazon’s stock is up 63% YTD and after the earnings call last week, the stock crossed our target price for the first time this year.

While the value opportunity has shrunk given the rapid stock price climb, Amazon is still one of the best run companies we have ever seen and continues to outpace its competition in the majority of its business lines.

As the company continues to hit its goals this year, we are looking forward to the massive numbers Amazon will post in the coming quarters.

Investment research disclaimer: the financial valuation methods, target prices, and model assumptions discussed above are for educational and informational purposes only and reflect only our views at the time of publishing. The information and/or strategies above should not be used to make investment decisions. Past results are not predictive of future performance and future investment proceeds are not risk free and cannot be guaranteed. We are not a registered investment advisor or broker and all investment decisions must be made independently of the educational research published here.