Earnings Analysis: Amazon Q1 2023

Summary: Everything was going well for Amazon until their CFO said one sentence during the earnings call that tanked the stock more than 10%. More on this later.

Overall, Amazon had a strong quarter and they are back on track. The company grew revenue faster than expected, improved operating margins, and scaled back capital expenditures. Our long-term expectations remain unchanged and our price target is essentially the same as last quarter.

Previous price target: $134.27

New price target: $134.75

Current stock price: $103.63

Headlines

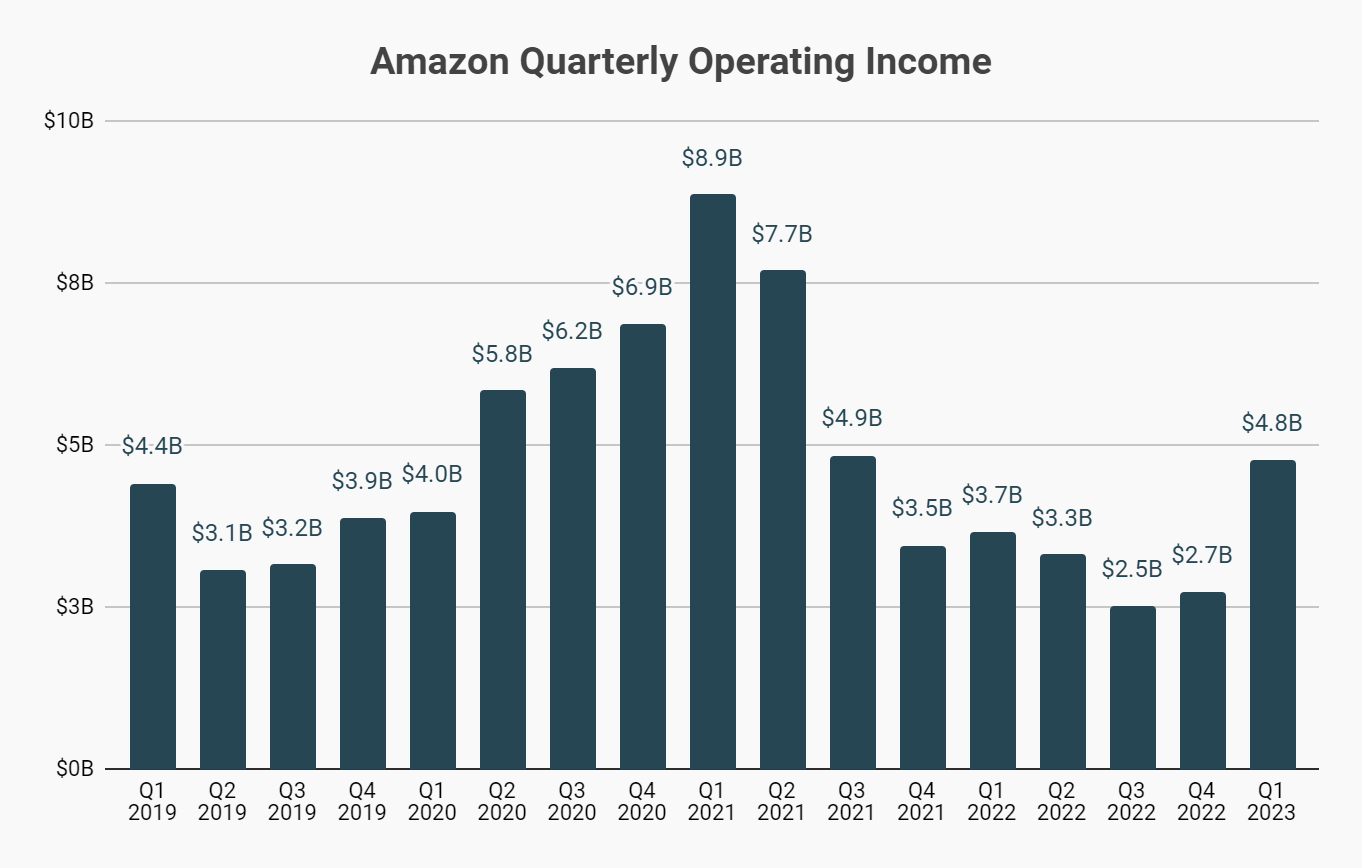

While most investors focused on Amazon’s strong revenue, we are focusing on operating income. The company made almost $5 billion in operating income which exceeded their Q1 2019 level. Why is this important?

We believe this quarter will mark the start of many quarters of strong operating income growth as Amazon undergoes several company-defining changes:

Corporate layoffs. The company is in the middle of laying off 27,000 corporate employees. While this is unfortunate for the impacted employees and their families, from a business perspective, this will benefit operating margins by several percentage points.

Regionalizing fulfillment centers. After doubling ecommerce warehouse space during the pandemic, the company is now finding ways to best utilize the network. Over the past several months Amazon has changed US ecommerce operations to a regional network, which will stock all items at the regional level instead of the country level. This will improve delivery times and save billions in fulfillment costs.

Focus on product ROI. Amazon’s executive team said they are analyzing every product and department within the company to identify long-term profitability prospects. The results of the analysis are now clear: Amazon’s Alexa, Twitch, and retail stores have all faced massive cuts. These areas likely had little promise of reaching solid long-term profitability so they are being scaled down to appropriate investment levels where they have a greater chance at profitability. The focus on ROI at the product level will also save the company billions annually by reducing investments in areas with little long-term promise.

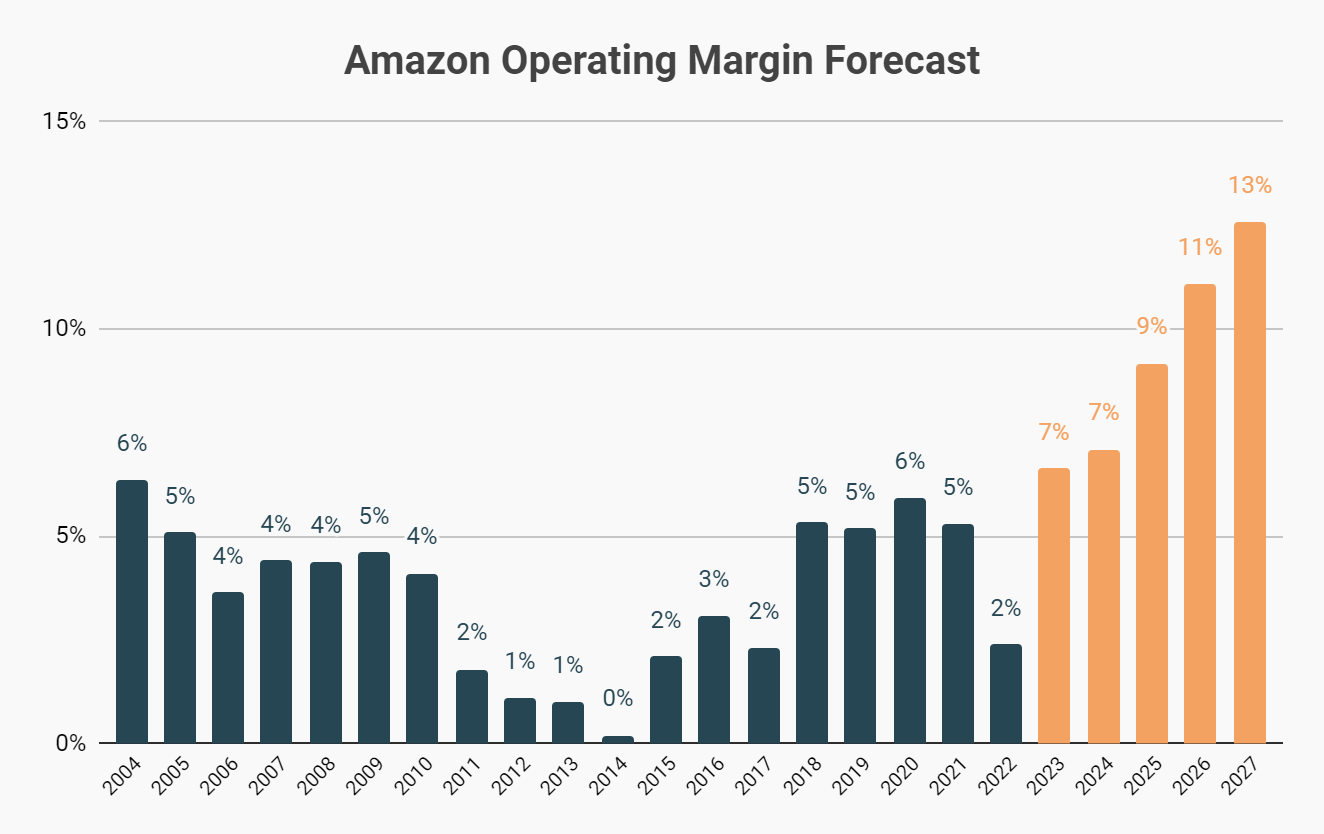

All told, we expect these changes to 6x Amazon’s operating margin from 2% in 2022 to 13% by 2027, which would be Amazon’s highest operating margin in their history.

Our Thesis

We believe Amazon is changing their long-term strategy to focus on near-term profitability instead of reinvesting profits back into the business which defined the company for their first 25 years of business.

Amazon’s profitability has tanked since Andy Jassy took over as CEO two years ago. This was not his fault as Amazon spent the past decade investing billions of dollars into projects like Alexa and tens of billions into increasing fulfillment capacity. Jassy has been vocal about the company’s lavish spending before he took over as CEO and his actions of selling warehouses and cutting back product initiatives speak volumes on the company’s new direction.

Jassy now wants to turn Amazon into a cash flow juggernaut and we think he will. Years of upfront spending on fulfillment operations will reap significant benefits in the coming years. And cuts to non-profitable business units will be immediately visible on the bottom line this year.

If successful, this strategy pivot will be a monumental moment in Amazon’s history and will unlock significant shareholder value in the long-term.

We are following Amazon’s business strategy very closely this year and will be tracking the following metrics over the next few quarters to see how the company is progressing:

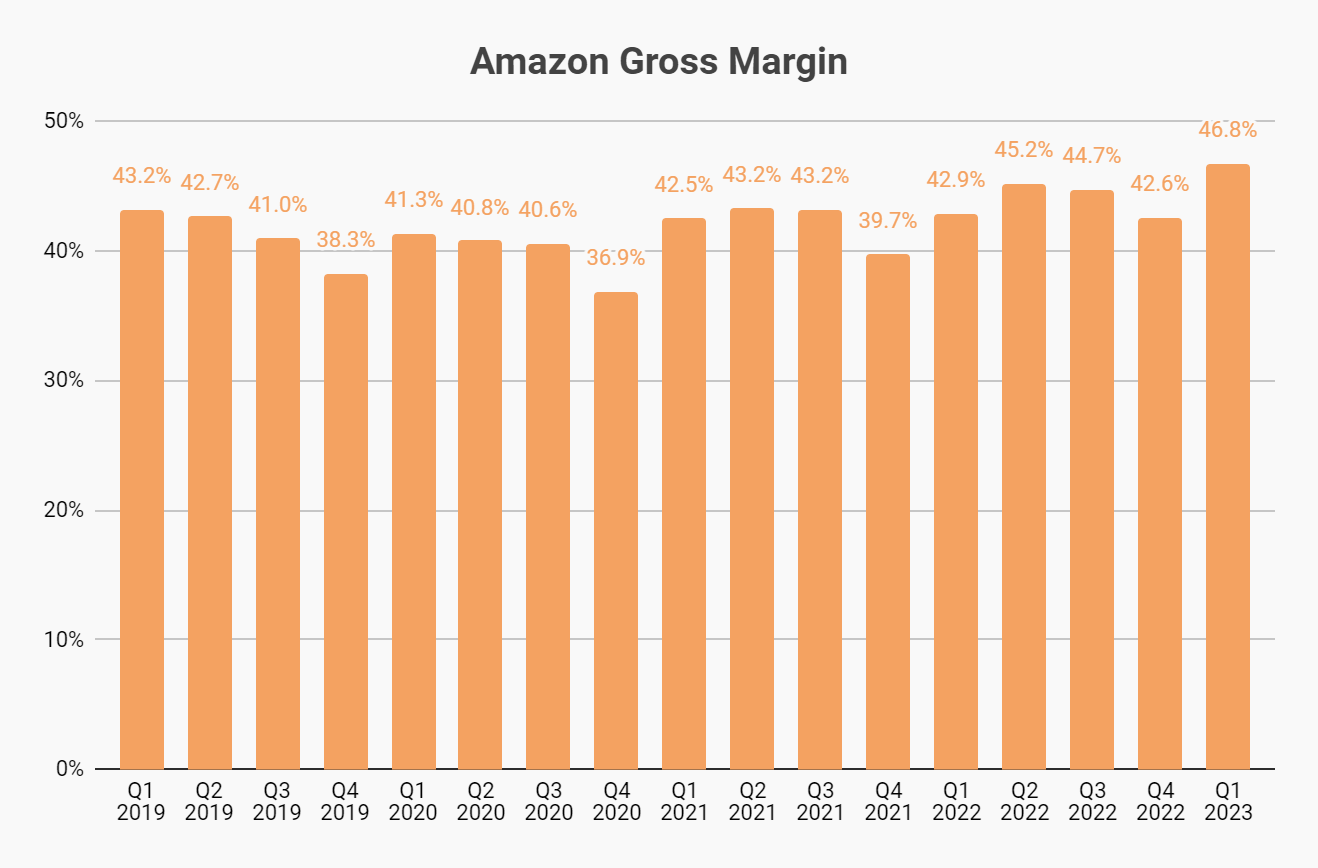

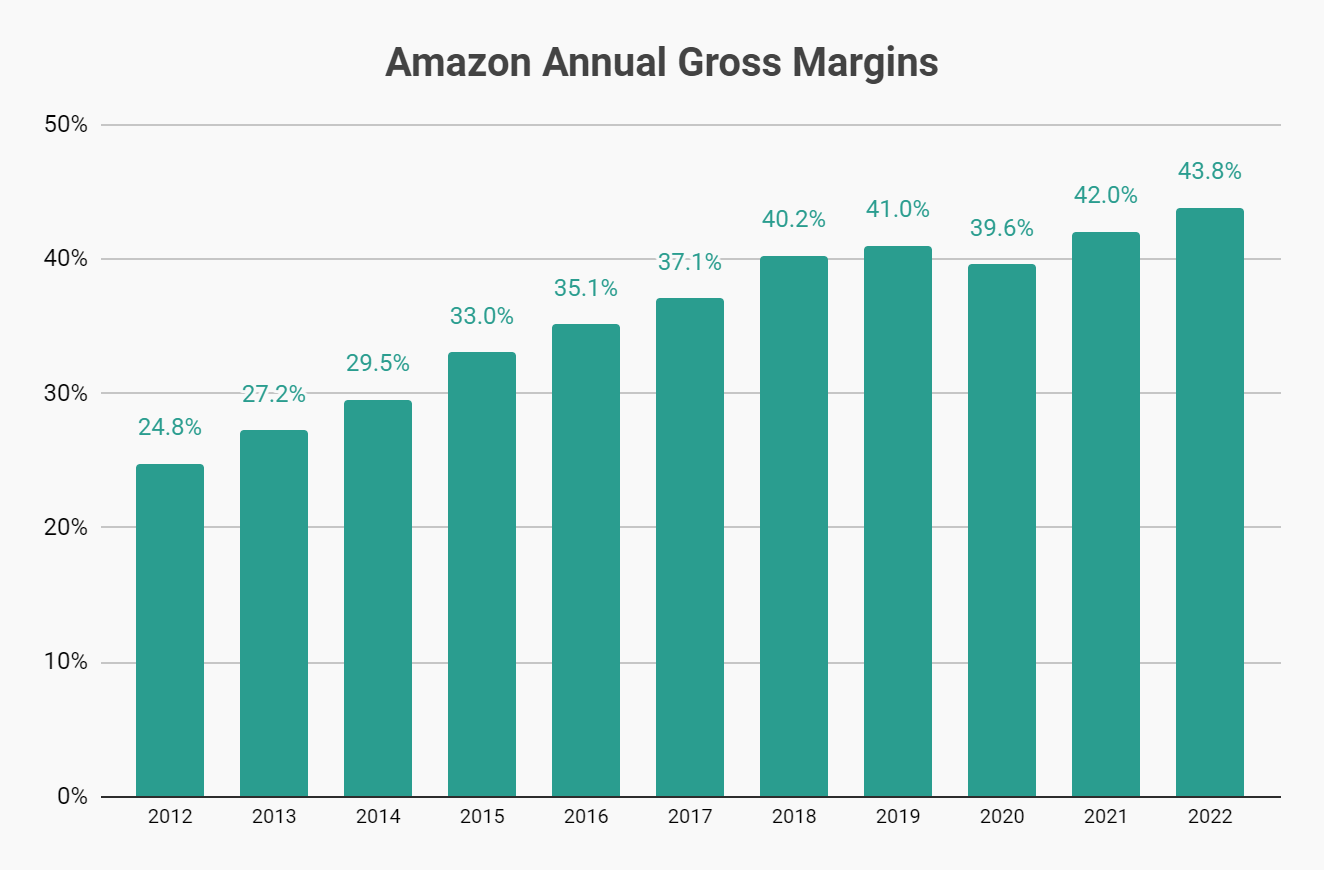

Amazon’s gross margin has likely improved as high margin segments (advertising, third-party services, and AWS) continue to grow faster than the company’s lower margin segments (online stores and physical stores). While Amazon does not provide gross margins at the segment level, we are pretty certain that advertising margins are better than grocery store margins.

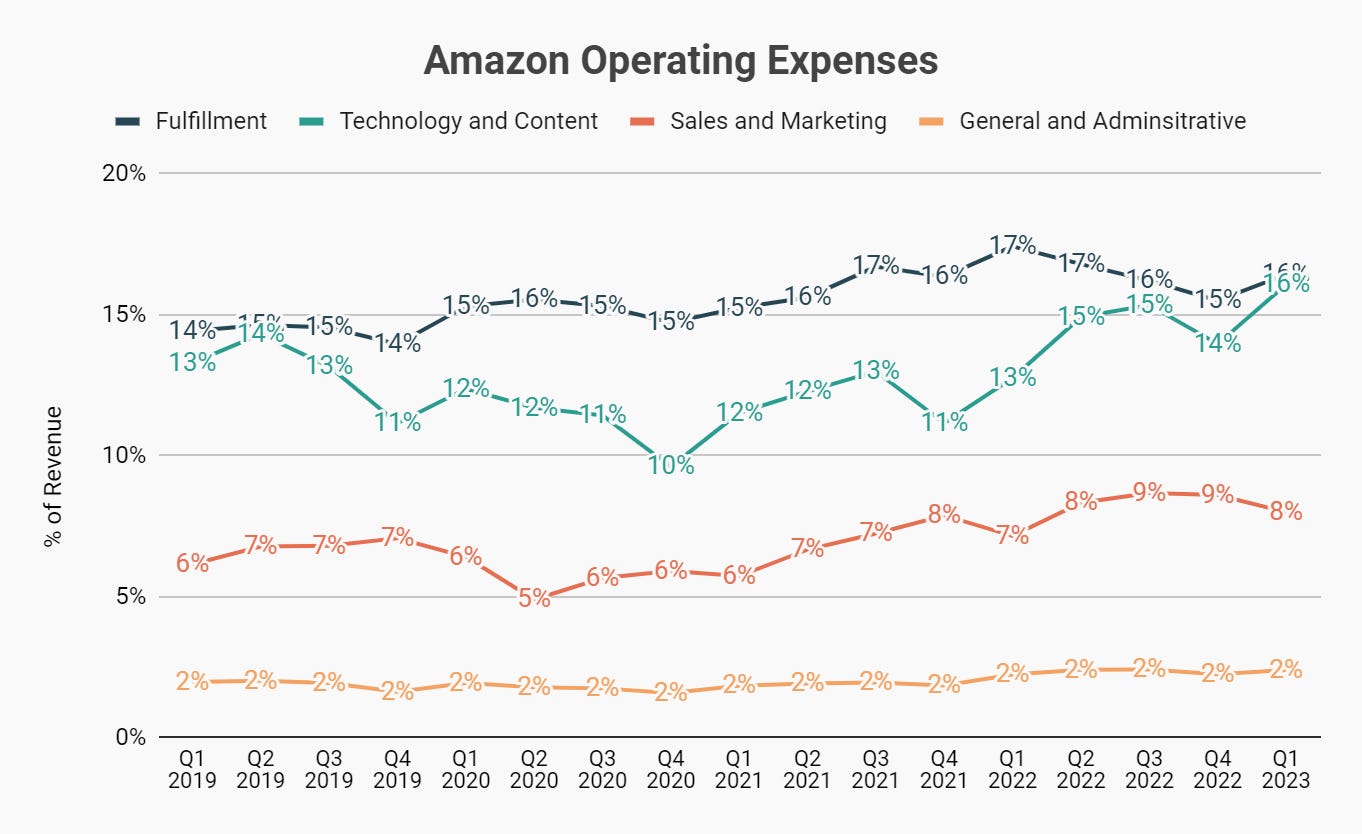

Operating expenses are the second component of a company’s expense base. For Amazon, operating expenses include warehouse fulfillment costs, engineering salaries, advertising costs, and overhead headcount and office buildings.

We mentioned that Amazon is reorganizing their fulfillment network so we are going to keep extra eyes on that blue line at the top of the chart over the next several quarters. We may already be seeing some benefit of their new fulfillment strategy as the company shipped 8% more products last quarter compared to Q1 2022 and fulfillment costs only increased 3%, implying strong cost leverage benefits.

For technology and content costs, we know this number will decrease as the company finishes layoffs in several product areas and AWS. However, this line item may not decrease until Q3 as severance charges will temporarily increase costs in Q2.

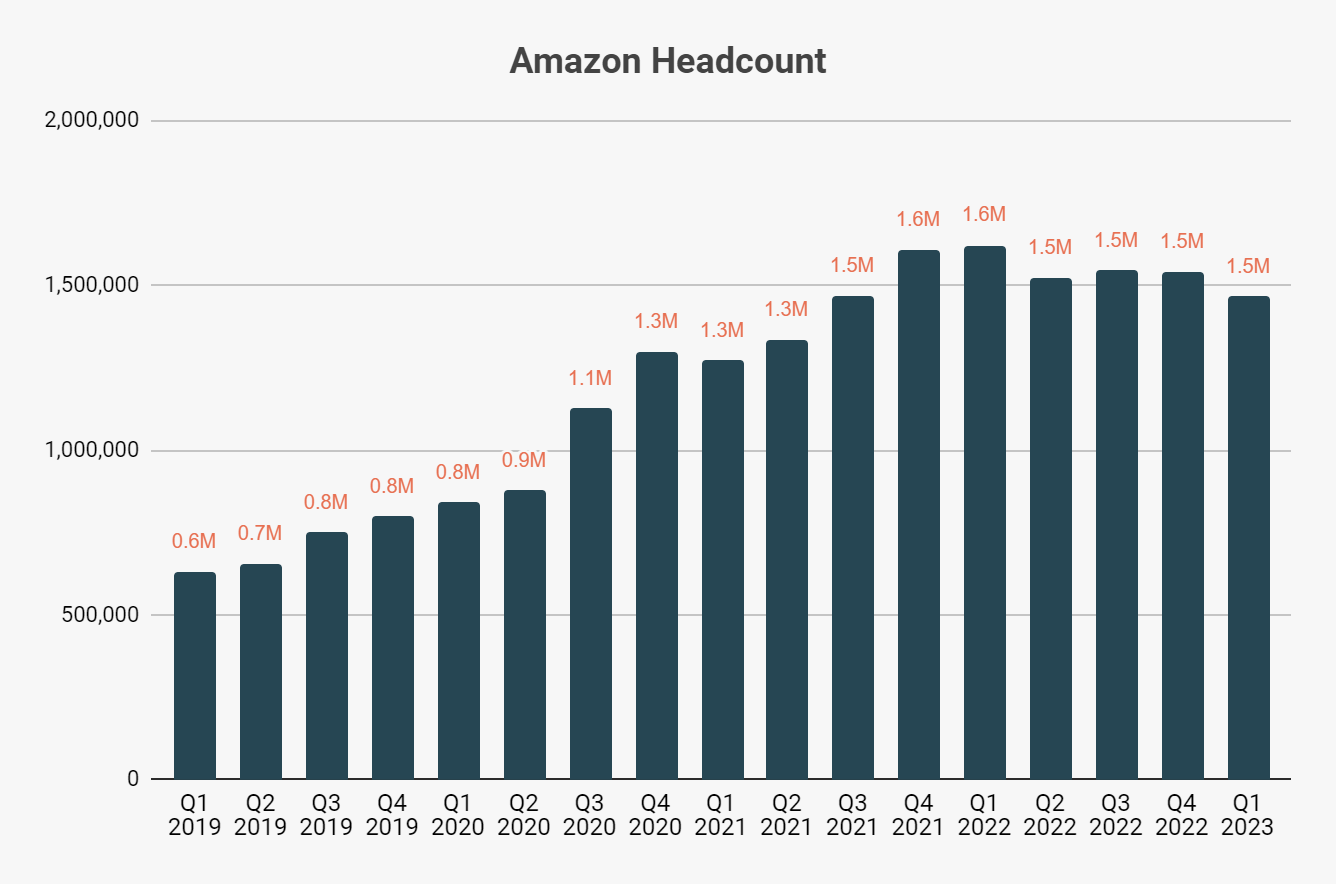

We estimate that employee salaries and benefits make up 65-70% of Amazon’s operating expenses. After almost tripling headcount from 2019 to 2021, Amazon is starting to reduce staffing at the corporate and warehouse levels.

The corporate cuts, nearing 27,000 employees in total, will save Amazon between $5-$10 billion in annual costs. The company is also optimizing their warehouse network to ship more products using fewer workers. It will be fascinating to see how low Amazon can keep their headcount even as they continue to grow.

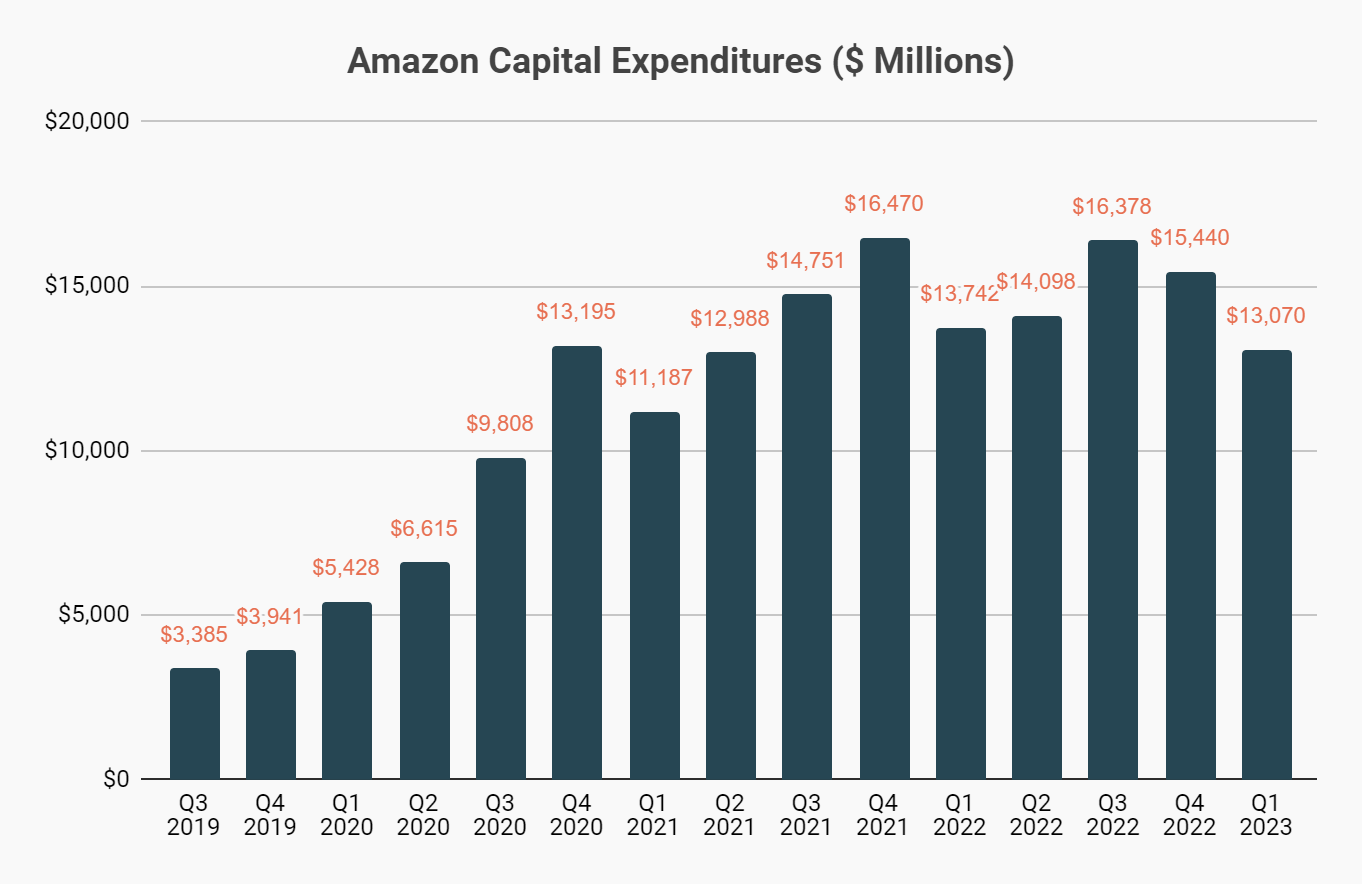

Lastly, we have capital expenditures, which are the costs Amazon spends upfront on new warehouses, data centers, office space, and equipment.

We mentioned earlier that Amazon spent tens of billions to add warehouse capacity in order to meet demand during the pandemic. Now that Amazon is under-capacity, the company has said that capex spending in the consumer division will decrease.

However, total capex spend it projected to remain flat as the company increase capex spend on AWS, which requires tremendous spend on data center equipment to keep the business running.

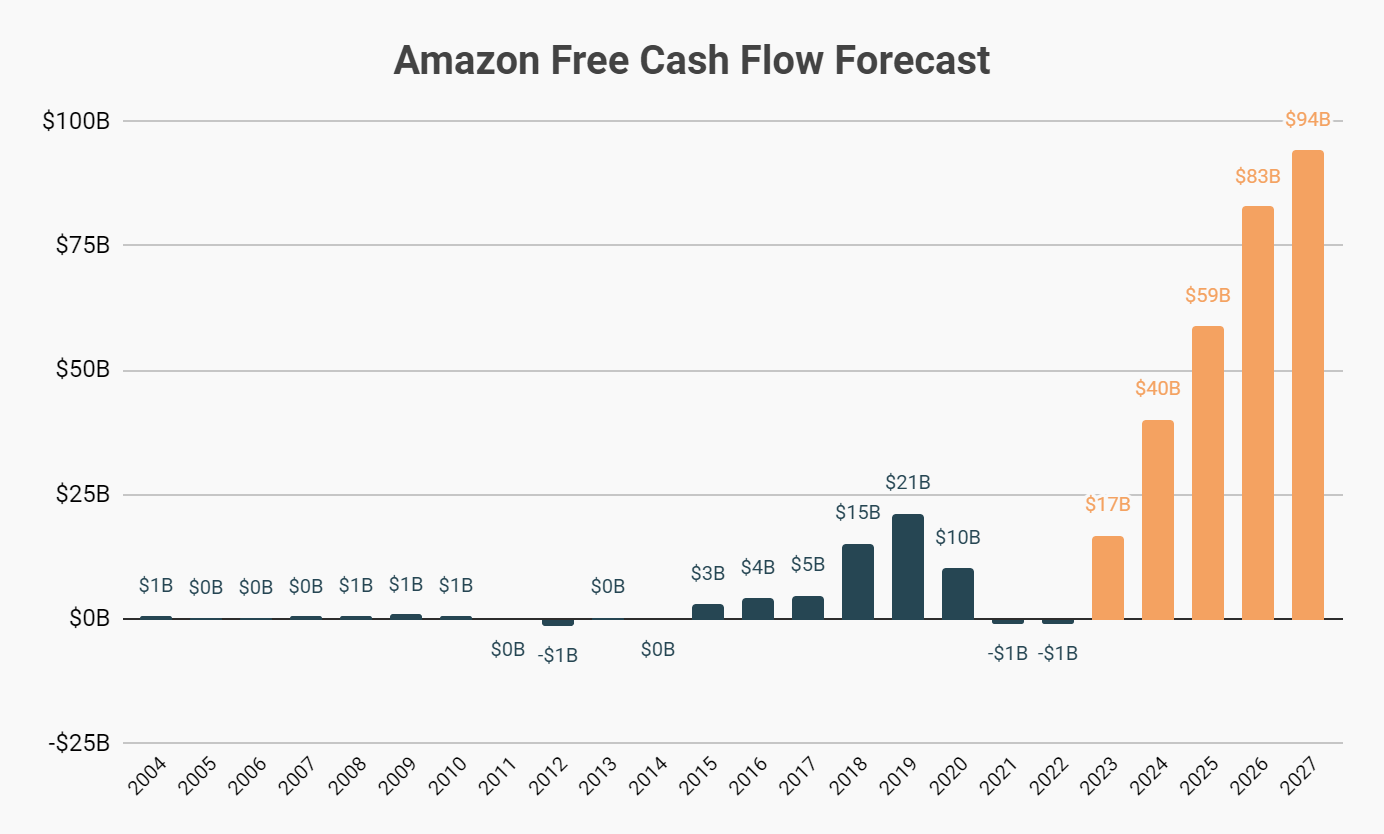

Capital expenditures is one of the most important pieces in calculating free cash flow and Amazon’s ability to control it will play an outsized factor in how much free cash flow they generate.

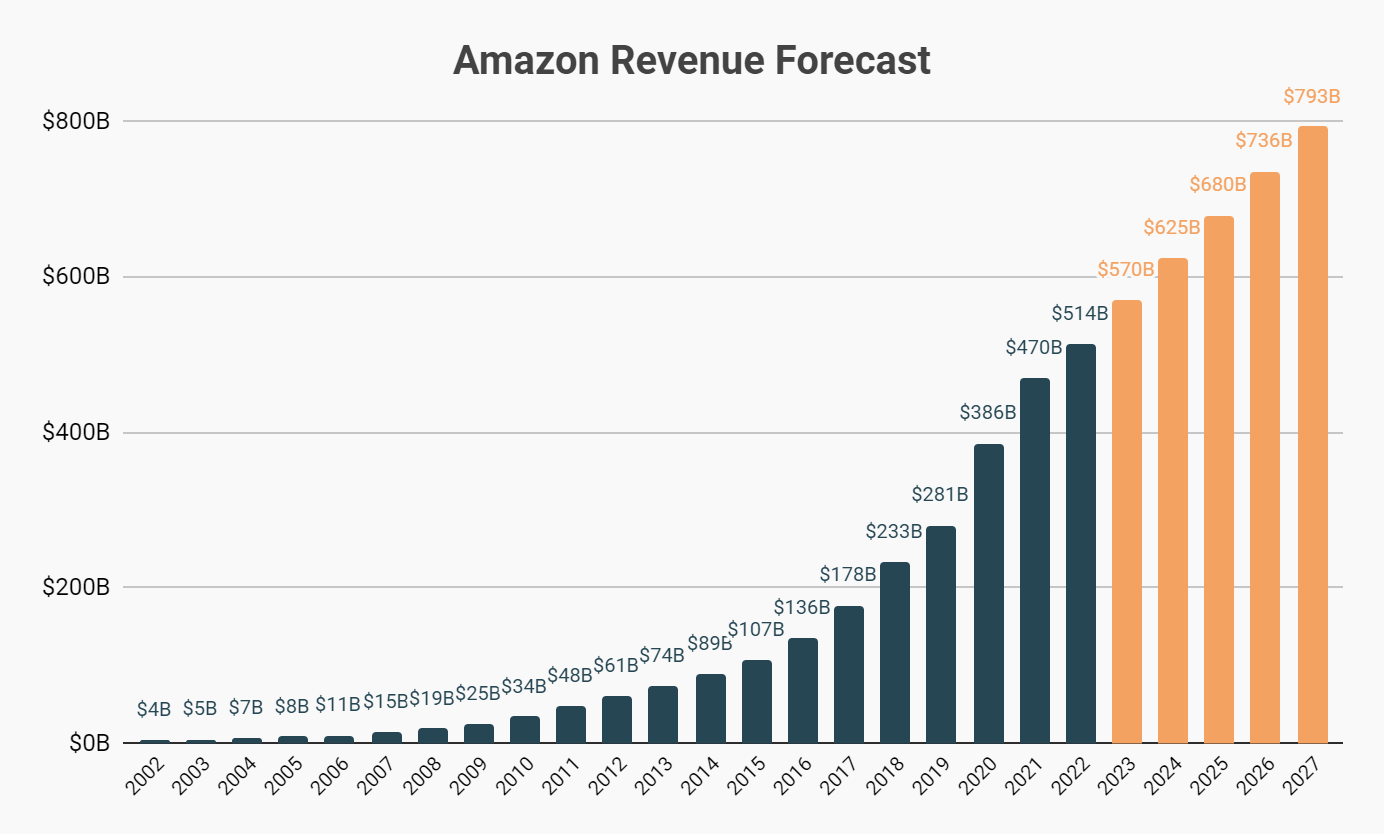

Revenue

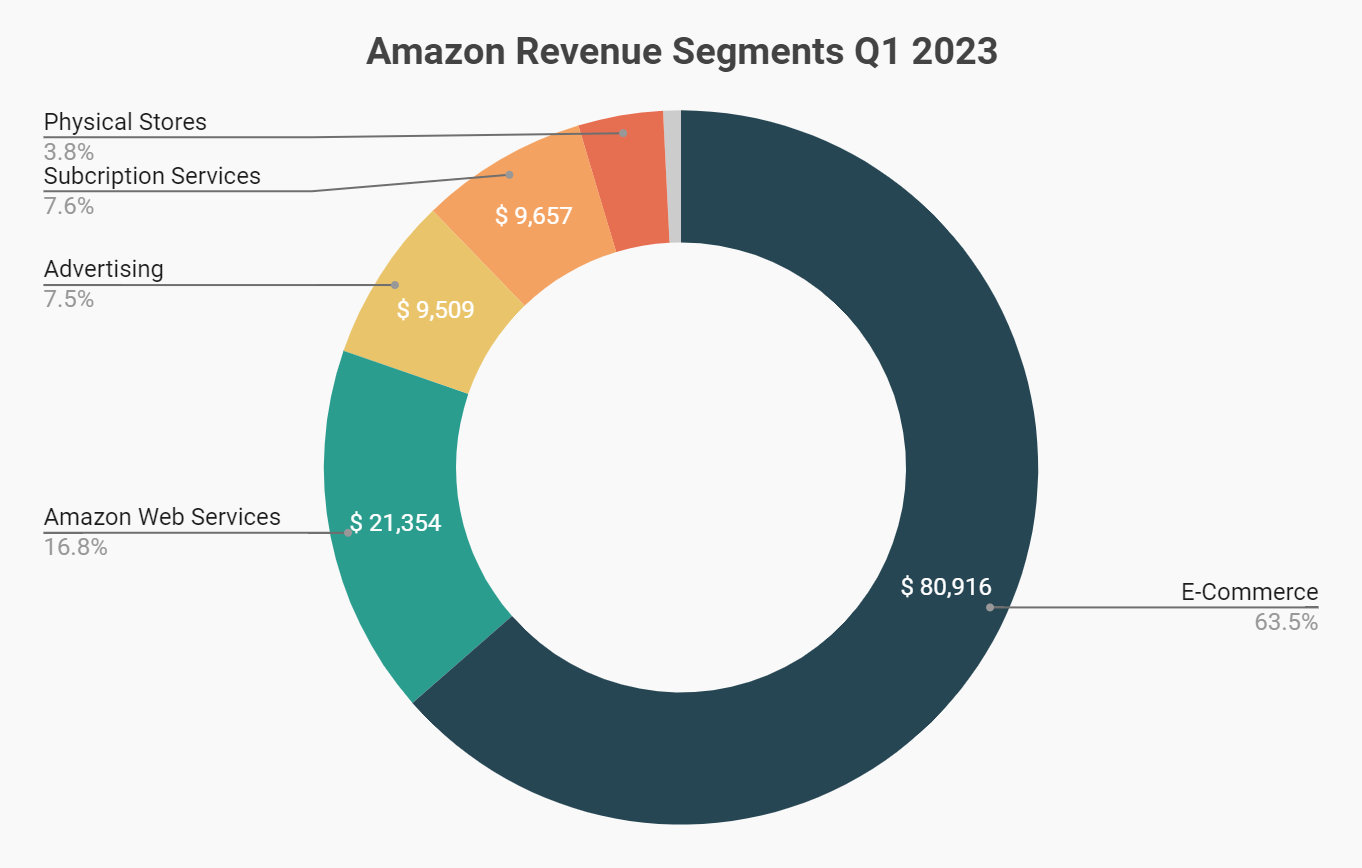

Let’s change gears to revenue growth. Amazon beat revenue expectations as segments like third-party seller services and advertising performed well.

The strong growth in non-ecommerce segments has changed Amazon’s business model over the years to a more diversified revenue model.

Amazon’s retail business (online stores, third-party seller services, and physical stores) now make up “only” 67% of the company’s revenue, compared to 75% in 2019 and 80% in 2018. This trend will only continue as AWS and advertising continue to grow faster than the retail business.

Not only does this diversify Amazon’s business model, it also improves the company’s profitability as the non-retail segments have significantly better margins than the retail business. We can see the trend of increasing gross margins as Amazon diversifies away from retail:

Amazon Web Services

In the first sentence we hinted that Amazon’s CFO may have tanked the company’s stock by 10% in the earnings call. This was because Amazon released their earnings 90 minutes before the earnings call and the results were so good that the stock climbed 8% within minutes.

Then came the earnings call. Amazon’s CFO Brian Olsavsky was discussing how AWS customers have been cutting back on AWS spend as they optimize their cloud costs and that this trend was continuing in April: “And we are seeing these optimizations continue into the second quarter with April revenue growth rates about 500 basis points lower than what we saw in Q1."

Why did Amazon’s stock drop 10% because of this one line? Investors love growth and anytime they hear growth declining, they panic. Every time.

We believe the panic was overdone. AWS, like all cloud providers, is seeing slowing growth as companies look to cut costs in any way possible. This is undoubtedly impacting AWS’s revenue growth this year but has little impact on AWS’s long-term prospects.

Businesses are continuing to move compute spend into the cloud and as the largest cloud provider, AWS will continue to benefit from this seismic industry shift that is still in the early stages. By working with AWS customers to reduce cloud spend, the company is managing relationships for the long-run.

Valuation

With all of that said, let’s get to the good part. Our price target for Amazon is $134.36 which is 30% higher than the current share price.

We have made our thesis clear: we believe Amazon will grow free cash flow significantly by continuing to grow its high margins business segments while reducing operating expenses through layoffs and optimizations.

We are forecasting 8-11% annual revenue growth for the next five years, driven by third-party seller services, AWS, and advertising.

On the free cash flow side, we are projecting serious growth.

While this may look extreme, we are projecting 2023 free cash flow to still be below 2019 levels. Prior to the pandemic, Amazon was just starting to generate significant free cash flow as they grew FCF 4x in just two years. They were then setback several years as they invested heavily in their warehouse network and AWS.

These investments should now pay off starting this year. This quarter, Amazon generated almost $2 billion in free cash flow compared to just $300 million in Q1 2022. And the $2 billion doesn’t even account for the savings from the layoffs, which are currently ongoing.

For the valuation, we are using a 10% discount rate on all future cash flows which leaves us with an enterprise value for Amazon of $1.4 trillion. The company is currently close to net debt neutral, with ~$65 billion in both cash and debt so our equity value is also ~$1.4 trillion. With 10.3 billion shares outstanding, this comes out to $134.75 per share.

We believe the company is on track to grow cash flows in a way that we have almost never seen before and we are excited to watch what unfolds in the coming years.

Investment research disclaimer: the financial valuation methods, target prices, and model assumptions discussed above are for educational and informational purposes only and reflect only our views at the time of publishing. The information and/or strategies above should not be used to make investment decisions. Past results are not predictive of future performance and future investment proceeds are not risk free and cannot be guaranteed. We are not a registered investment advisor or broker and all investment decisions must be made independently of the educational research published here.