12 Years of Costco Under CEO Craig Jelinek

Costco announced yesterday that Craig Jelinek would step down as CEO after 12 years at the helm. In his 12 years as CEO, Costco’s stock has grown 9x including dividends, more than double the return of the S&P 500. Let’s take a look at the numbers behind Jelinek’s run at Costco.

Revenue

For uninitiated, the chart below may look normal. It shows a business growing revenue by about 9% per year, no big deal right?

There are very examples of a company growing revenue consistently at this scale. Costco went from a $142 billion to a $242 billion business in just five years, which is remarkable in a world of in-store retail.

So what is driving Costco’s revenue?

Costco calls their stores “warehouses” and they only have 861 of them. Craig Jelinek continued Costco’s strategy of only opening new warehouses when they were 100% ready to support it. The company staffs new warehouses with experienced leaders internally and they will only open a new warehouse when they feel they have the proper mangers in place.

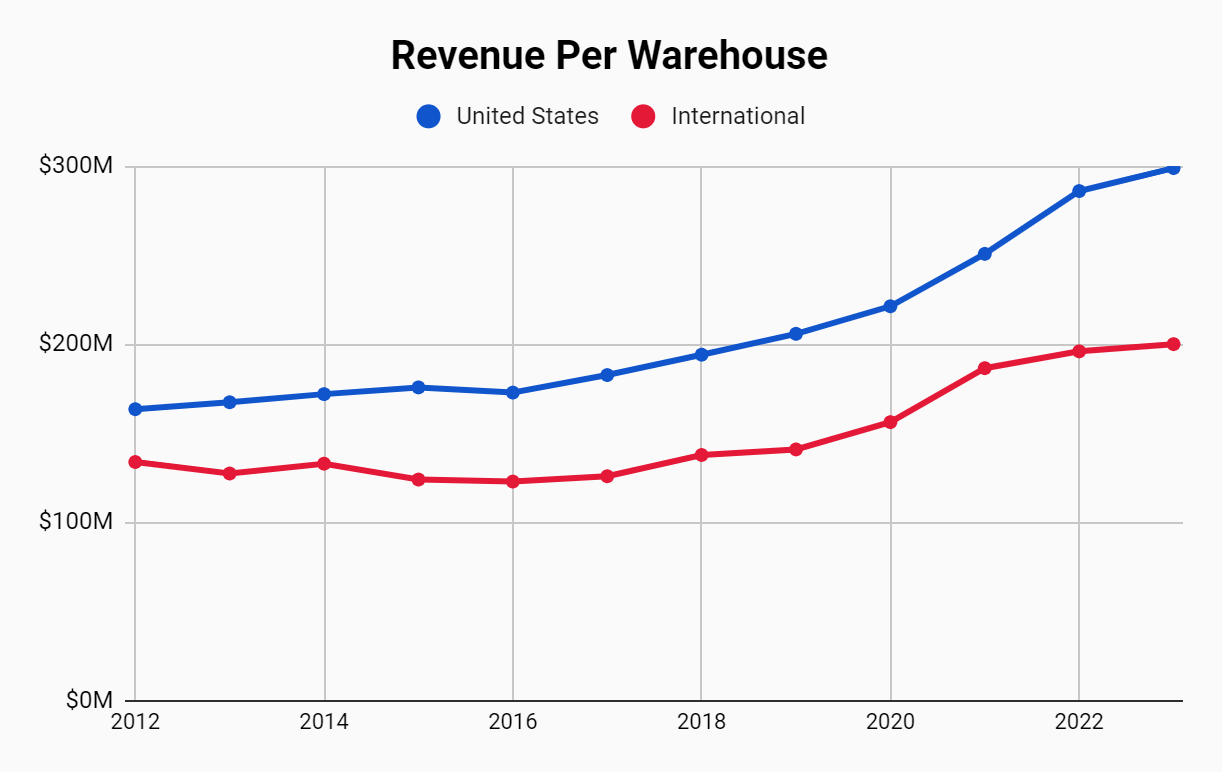

You can imagine those 861 stores put up numbers. $300 million per US store to be exact. To put that into perspective - Costco has 33 stores in Washington state, so those 33 stores alone will do more revenue than all of Airbnb in one year.

Costco tackled the economic conditions of the past three years head on. On the revenue front, same store sales hit unprecedented levels as consumers flocked to Costco warehouses to stock up on food and household items.

If you’re a Costco customer that probably won’t surprise, their warehouses are busy almost 24/7.

Members

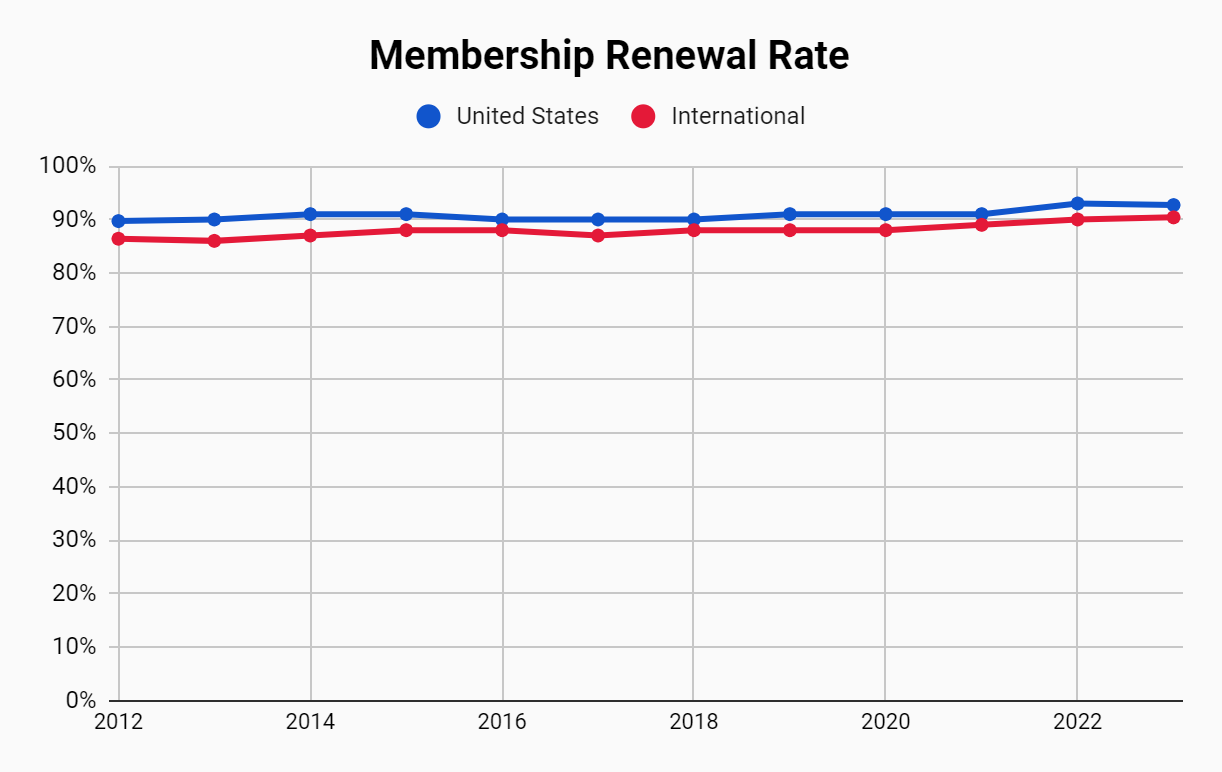

There is no denying that Craig Jelinek continued and built upon Costco’s culture of customer obsession. More and more members are signing up for memberships even in warehouses that have been opened for decades. The main driver of this is the company’s sky high membership renewal rate.

Over 93% of US Costco members renew their memberships each year. That is unheard of for any membership business.

Expenses

Equally as impressive has been Costco’s ability to control margins in a time where almost every other retailer has struggled with margin suppression and inventory levels.

Costco’s gross margin “slipped” from 13.0% in 2019 to 12.2% in 2023 as the company continues to rigorously negotiate with suppliers for lower prices while holding their margin steady for their customers.

On the inventory side, Costco remains best in class. The company turns over inventory 12 times per year which is 2-3 times better than the average retailer.

Free Cash Flow

Here is the answer as to why Costco has outperformed the S&P 500 under Jelinek’s watch:

The first chart is Costco’s annual free cash flow which increased 4x from Jelinek’s first full year in charge.

The second chart shows the cash the company has returned to shareholders through dividends and stock buybacks.

Employees

We’ll end with a chart that Jelinek would love. The company employs 316,000 people around the world and most of them are happy to be employed by Costco.

Costco is one of the most employee friendly employers in the retail world as they offer competitive wages, internal opportunities, with strong benefits.

To replace Jelinek, the company has promoted Ron Vachris to become CEO. Vachris has been with Costco for 40 years so we expect these charts will look almost identical when we look back 12 years from now.